Best Way to Get Out Of High Credit Card Debt (if you can’t afford to pay)

High credit card debt and loan interest rates are criminal. As a result, many of these credit card companies – big names like Bank of America, Chase, Discover, and Citifinancial – get sued for millions of dollars per year for their lending practices. Of course, the best way to deal with high credit card debt is using the same unreputable lending practices that banks use against you, but we’re using them to help you fight the debt and not have to pay it. So let’s take a closer look.

Are you only making minimum payments each month?

About 90% of people with debt make minimum payments, so you’re not alone. But, unfortunately, it’s a pay forever plan where all you do is pay interest and penalties, and it can take 17-20 years of making minimum payments to get out of this situation. Have you looked at the payoff dates on your statements?

Please take a deep breath and relax because we’re about to give you some options to relieve you of this debt and stress.

Debt validation programs can be one of the best ways to deal with high credit card debt. Validation can be especially effective for consumers that can’t afford to pay their balances “in full” every month due to low or no income.

The issues associated with the credit card industry have been legally defined as unfair, deceptive, and even predatory. If you remember how you originally received the credit cards, it probably went something like this:

- You received a solicitation in the mail

- It offered you a low interest rate

- It also offered you a “pre-approved credit limit” of thousands and thousands of dollars.

Next, you probably:

- Were asked to write down some personal information and perhaps how much money you make

- Then you dropped the offer in the mailbox.

- And a few weeks later, “POOF,” you got a card in the mail with a nice big credit limit.

Does this sound about right?

Well, that is precisely where the issues began. First, the creditors did not properly qualify you for the credit card.

Have you ever bought a home, a car, or anything else requiring credit without filling out an extensive credit application?

Then why now?

Credit cards should require an application. Additionally, there’s something unique about credit card accounts. They are the only type of account where the creditor makes more money if you go late and cannot pay back the credit extended to you. If you go late on your mortgage or car loan, your interest rates don’t triple, do they?

This is where the validation comes into play. It ensures you do not pay on a legally uncollectable account.

Now, most of the work in this process begins when your account is with the collection agency. Therefore, your accounts need to be with the collection agency for this program to work, which means they will typically be 90-120 days past due. Rest assured, after the account is invalidated; it can no longer legally remain on credit reports. So for no extra cost, the validation program offered through Golden Financial Services includes credit repair.

Call (866) 376-9846 to see if you qualify and learn all of your options. Get a free consultation from one of our experienced debt counselors.

How the debt resolution (i.e., debt validation) program can help resolve high credit card balances:

After you’re approved for the program:

- When you receive a collection letter for one of your accounts, you must immediately send it to the debt resolution program.

- The debt resolution company will prepare a dispute package that gets sent to each collection agency legally, demanding proof of their right to collect on the account.

- If the collection agency cannot verify their authorization to collect, the account is classified as invalid and unable to be collected upon. According to Golden Financial Services, “Collection agencies are unable to verify their authorization over 75% of the time.”

- During the program, you are introduced to a law firm to provide you debt collection and credit education. In addition, that law firm will provide you legal protection if your legal rights are violated while on the program. You will also receive credit restoration for no additional cost. That means after each debt is invalidated, the credit repair will dispute the account on your credit. In addition, during the first several months of the program, the credit repair will work together with you to dispute any inaccurate or outdated information on your credit report for no extra cost.

Now there are several reasons why the collection company does not have legal right to collect on these accounts; the two most common are:

- The creditor did not properly qualify you for these accounts.

- The original creditors cannot give the collection agencies important documentation that is legally required to collect on a debt due to privacy laws. Without this documentation, the collection agencies do not have the legal right to collect on the debt. Bill collectors must abide by all Federal & State laws, statutes, and guidelines to have the legal right to collect on your accounts.

Why do collection agencies try to scare people when collecting on debt?

Collection companies are completely aware they have no legal right to collect on a debt. So, they use scare tactics instead of taking the proper steps to follow the law because it is too time-consuming and expensive for them to do so. It is a numbers game for them, just like the credit card companies.

What if a debt is proven valid (i.e., validated and verified legally collectible)?

Suppose an account is verified to be legally collectible and valid. In that case, one of our A+ BBB accredited debt settlement partners negotiates with the collection agency to settle the debt for less than the full balance. In the end, the programs offered through Golden Finacial Services ensure your debt is resolved, and you end up paying less than the full balance on each account enrolled. Our process prioritizes saving the clients money and helping them plan to rebuild their credit.

The author of this post is Paul J Paquin, the CEO of Golden Financial Services.

If You’re Buried in Credit Card Debt and Don’t Know What to Do

At this point, it can feel as if you hit a brick wall. But the good news is, debt validation can offer you a solution.

Just remember, it’s not your fault that financial hardship occurred. Medical conditions, divorce, loss of income – these incidences are all unexpected in most cases.

Ordinary people don’t plan to save for unforeseen medical expenses – or divorces – or layoffs. So, when these types of conditions occur, people are caught off guard and often use credit cards to pay the bills.

Eventually, credit card payments become overwhelming, and at times unmanageable. Even worse, people will pay only minimum payments and never get out of debt due to high interest.

Let’s look at the pros and cons of the different debt relief options out there.

Once we explain all available options to people, most will choose Debt Validation.

Validation will expose your creditors if they are illegally attempting to collect on a debt.

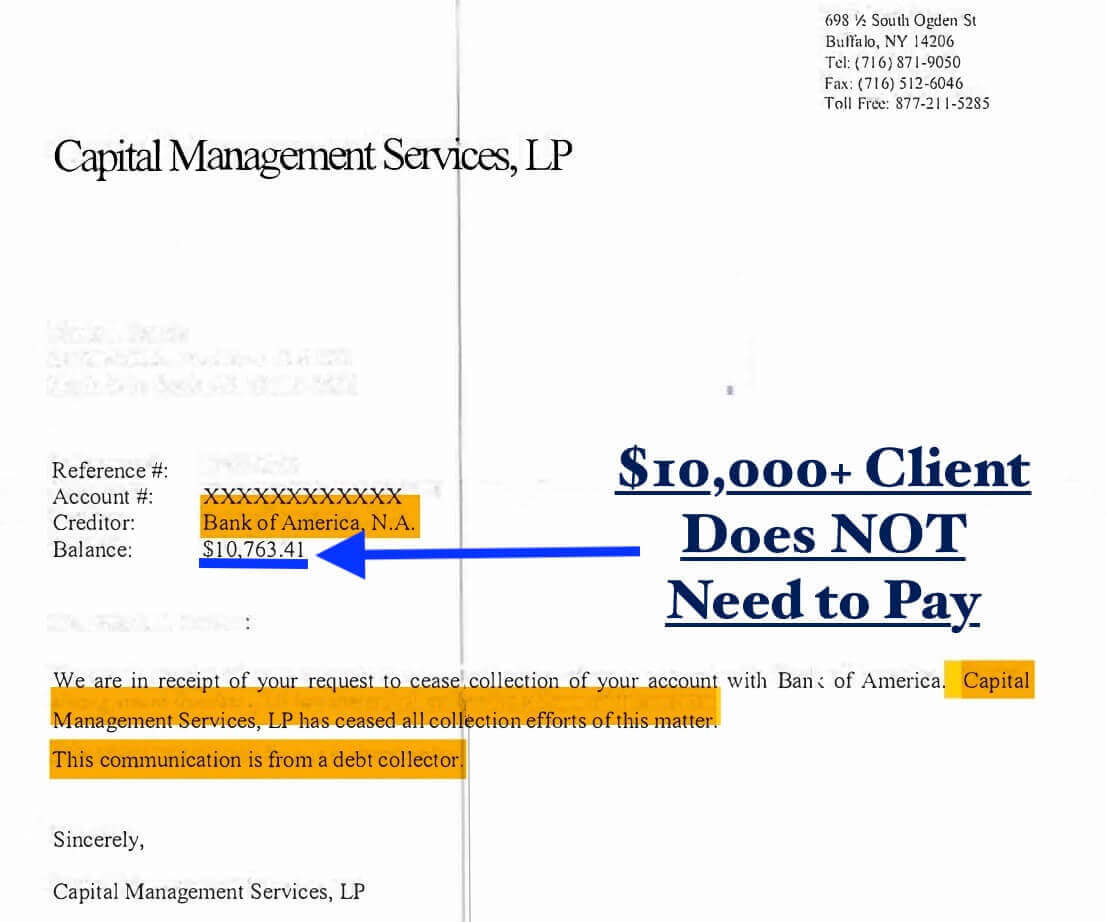

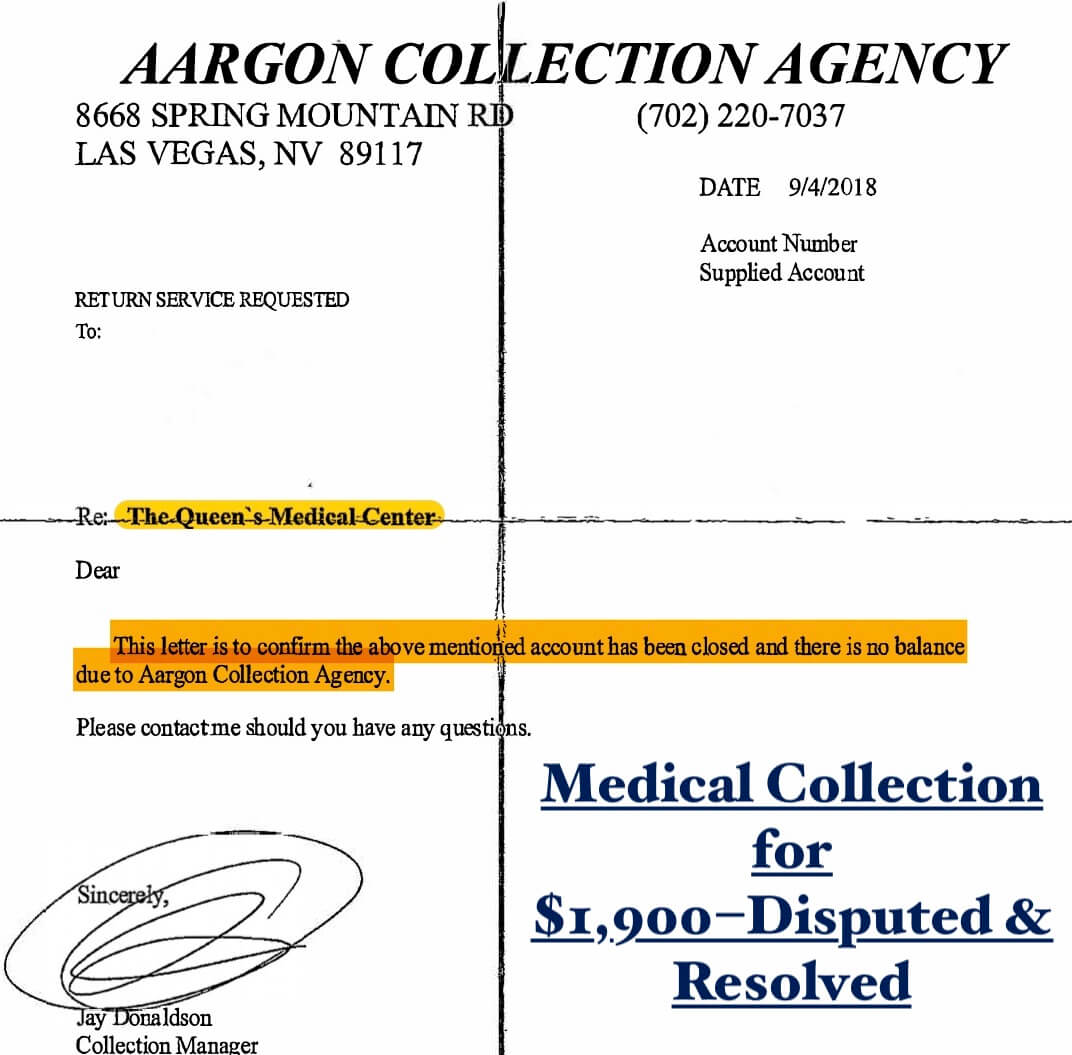

Here’s an example: The consumer used debt validation to resolve a Bank of America credit card debt that had a balance of over $10,000.

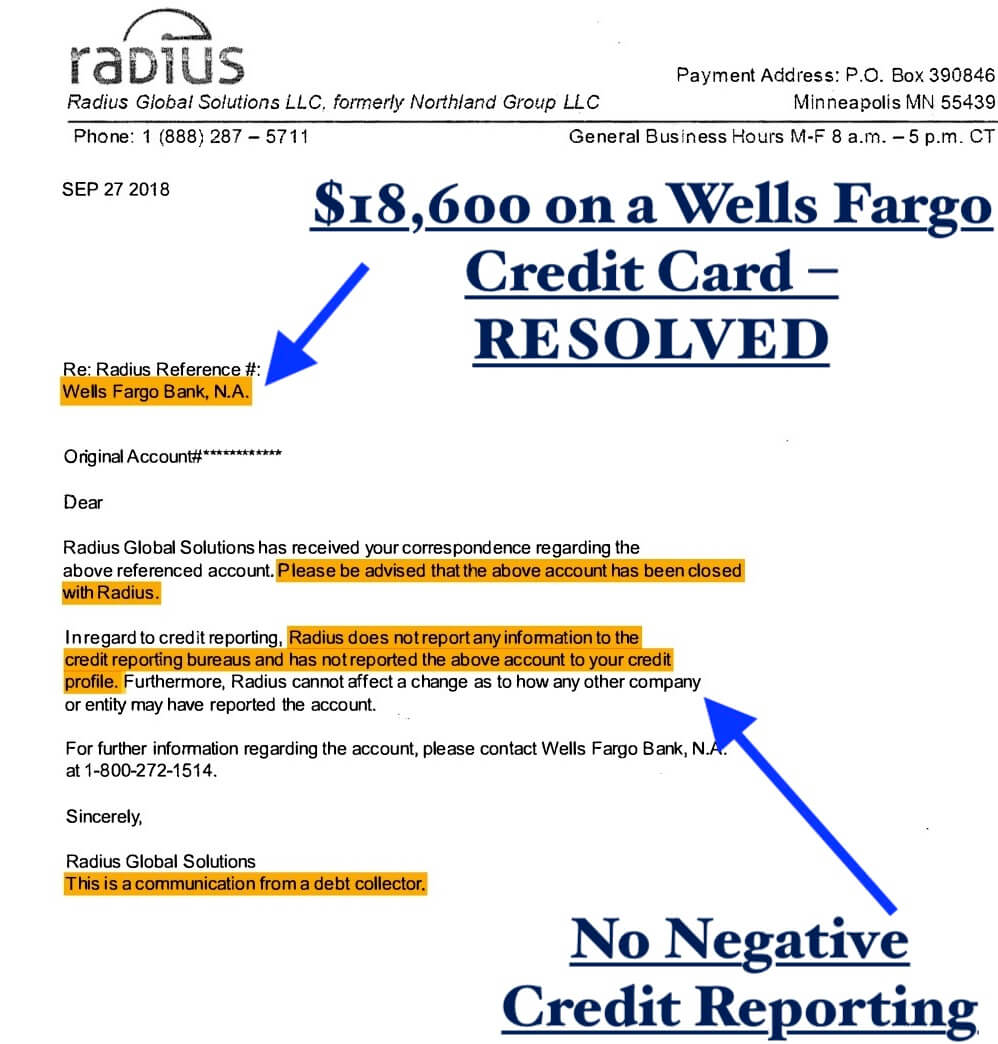

This next client could get out of almost $20,000 in credit card debt originally owed to Wells Fargo using debt validation.

What type of debt qualifies for a debt validation program?

- Citibank, Capital One, Wells Fargo, Bank of America, Discover, and almost all credit card debt.

- Medical bills and third-party debt collection accounts that have a balance of over $750. Almost all collection debt qualifies, including repossessions, Midland Funding, and Midland Credit Management.

- Almost any type of unsecured debt, including bank loans that have gone to collection status

- Financial company loans like Prosper

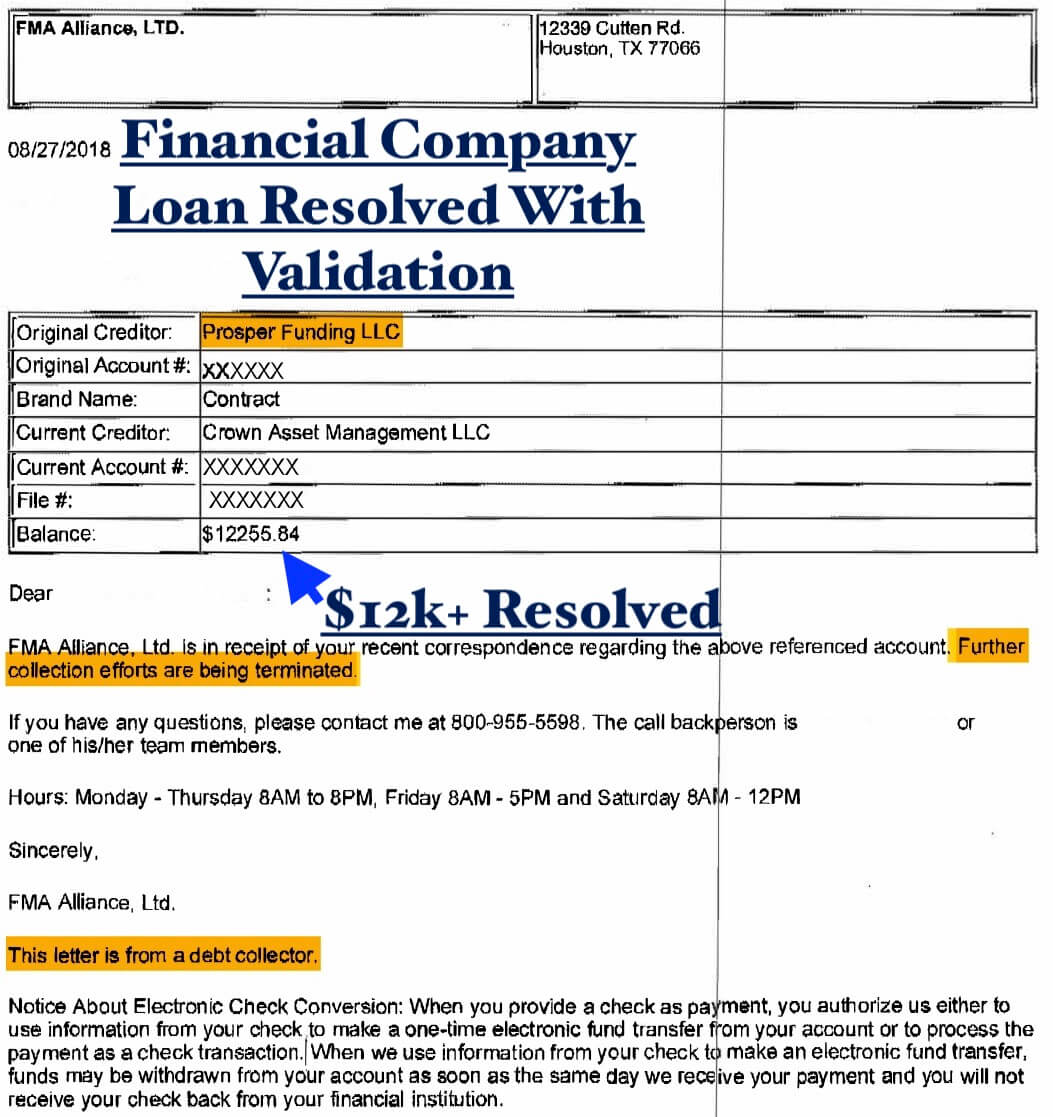

This next client was able to resolve a high-interest personal loan from Prosper Funding, in the end, not having to pay it. The total debt amount was allegedly $12,255.84. After getting disputed with validation, the collection agency immediately agreed to stop collection on the account.

Here’s another example of a medical bill that was disputed and resolved by validation.

Why does debt validation work for so many kinds of debt with just about any consumer?

Have you heard the story about Felicia Tancreto?

American Express claimed that she owed $16,000 in credit card debt and even went as far as issuing her a credit card summons.

Noach Dear, a civil court judge in Brooklyn, later dismissed the lawsuit, citing a “lack of evidence.”

The American Express employee who testified “provided generic testimony about the way the company maintained its records. The same witness gave similar evidence in other cases.”

Following this case, it was concluded that “90 percent of credit card lawsuits are flawed,” meaning creditors can’t prove that a person owes the debt.

Judge Dear stated, “Lenders are churning out lawsuits without regard for accuracy and improperly collecting debts from consumers. The concerns echo a recent abuse in the foreclosure system, a practice known as Robo-signing.”

Banks use Robo-signing to produce similar documents for different borrowers without reviewing them, leading to inaccurate information.

As of 2021, lenders across the nation are facing significant scrutiny.

According to an article in the Washington Post, amongst other sources, “The Office of the Comptroller of the Currency is investigating JPMorgan Chase after an ex-employee revealed that nearly 23,000 past-due accounts had incorrect balances.” This investigation has been ongoing since 2011.

If your number one goal is to stay current on credit card payments without even a temporary dip in your credit score, debt validation is not the right option. First, let’s look at debt-relief options that don’t require you to be delinquent on payments. We will then continue talking about debt validation benefits below.

But in the meantime, keep this in mind if you are considering debt validation:

- 1.) Your credit score has already been adversely affected if your credit cards are all maxed out due to high balances. Therefore, people seeking debt relief services are often past the point of being concerned with their credit getting affected.

- 2.) Credit repair is part of the program.

- 3.) It only works because creditors so commonly engage in illegal practices.

Debt Relief Programs That Don’t Hurt Your Credit Score:

- 1.) Can I pay a credit card with a credit card?

Balance transfer cards offer you another way to consolidate debt. You can use a balance transfer card that offers a 0% interest rate for up to 18-months. If you pay off the balance within that 18-months, you can eliminate all interest.

Interest is a silent financial killer. Don’t let yourself fall victim to it.

You will pay an upfront fee with balance transfer cards that will cost approximately 3%-5% of the total debt amount transferred onto the card. So, for example, if you transfer $100,000 of credit card debt onto a balance transfer card, you could owe a $5,000 upfront fee.

- 2.) Should I get a consolidation loan?

Debt consolidation plans offer you minimum savings because you are only saving money on interest, at best.

How and Where to Get Loans For High Credit Card Debt:

- Must-Have a 700+ Credit Score to qualify

- Try to get one from a bank or preferably a credit union (due to low rates)

- Avoid most online lenders due to high fees (example: Lending Club and PayPal Loans for high credit card debt, come with high interest and additional fees)

- Click here to read more on how debt consolidation affects your credit

- 3.) Should I use Consumer Credit Counseling?

Besides using a loan to pay off debt, you can use a consumer credit counseling program that won’t negatively affect your credit score. However, this is another program that offers only partial savings.

More information on Consumer Credit Counseling

- 1.) This plan is only for credit card debt.

- 2.) You can become debt-free in 4.5 years

When it comes to debt relief, very few people choose these plans. You can save more on debt validation and negotiation.

How to Pay Off Credit Cards Fast?

When this question is asked, most debt relief companies quickly spill out some pitch about debt settlement.

The T.V. and radio ads that say “Call to Get Your Debt Forgiven” are referring to a debt settlement program.

But a debt settlement program should only be a last resort, used to avoid bankruptcy. After you settle a debt, your credit report shows the late and collection marks for up to seven years.

Since this program is so popular, let’s talk about this option first.

Debt Settlement to Pay Off High Credit Card Debt Fast

Debt settlement services let you pay off an unsecured debt for less than the full balance owed.

You get additional protection when using a law firm to settle your debt.

Golden Financial Services recommends using only an attorney-based debt settlement program.

There are two main reasons why:

- According to the Fair Debt Collection Practices law, if your creditors are told that an attorney represents you, they must now direct all communication to your attorney.

Since you won’t have to deal with creditor harassment, you will have additional relief.

- Credit card companies and debt collectors violate peoples’ rights all the time.

Why does this benefit you as the consumer?

When using a debt settlement law firm, the law firm educates you on consumer laws and debt relief.

The law firm will train you to spot and report any legal violations that your creditors commit.

An attorney can then use these legal violations as leverage when negotiating to reduce debt.

Attorneys can also sue a debt collection company for an FDCPA violation, where you could get awarded up to $1,000 per violation.

In some cases, an attorney can even use legal violations to get a debt dismissed, which only an attorney can do.

Debt Validation: The Program with Highest Savings

A debt validation program potentially lets you pay much less than if you were to settle a debt.

Debt validation can also get the debt and its associated negative marks removed entirely from your credit report.

Here’s a debt validation example letter:

Notice the creditor agreeing to release $4,376.39 of credit card debt and remove the entire debt from Experian, Equifax, and Transunion credit reports.

How debt validation can help you deal with credit card debt:

Debt validation challenges each of your debt collectors, forcing them to prove that they are legally authorized to collect on a debt and that what they claim you owe is accurate.

One of the main sources of revenue for creditors is the “fees” charged to accounts – late fees, over-limit fees, and annual fees. A fee that is inconsistent with the credit card company’s original agreement renders the entire debt invalid. Interest rate hikes work the same way. Credit card companies can increase rates if they do so consistent with the initial card-member agreement, but any deviation from that agreement and the debt is again rendered invalid.

Validation isn’t saying, “I never spent the money.” Debt validation is just making sure your creditors are abiding by the laws.

It’s difficult to imagine, but most of the time, a debt collection company can’t prove that they are legally authorized to collect on the debt. By disputing a collection account before agreeing to pay, you force the collector to verify and prove the debt is valid.

What happens after a debt is invalidated?

If a collection agency can’t validate and verify that they are legally authorized to collect on an account, they will need to cease all collection activity on the debt, and it becomes invalidated.

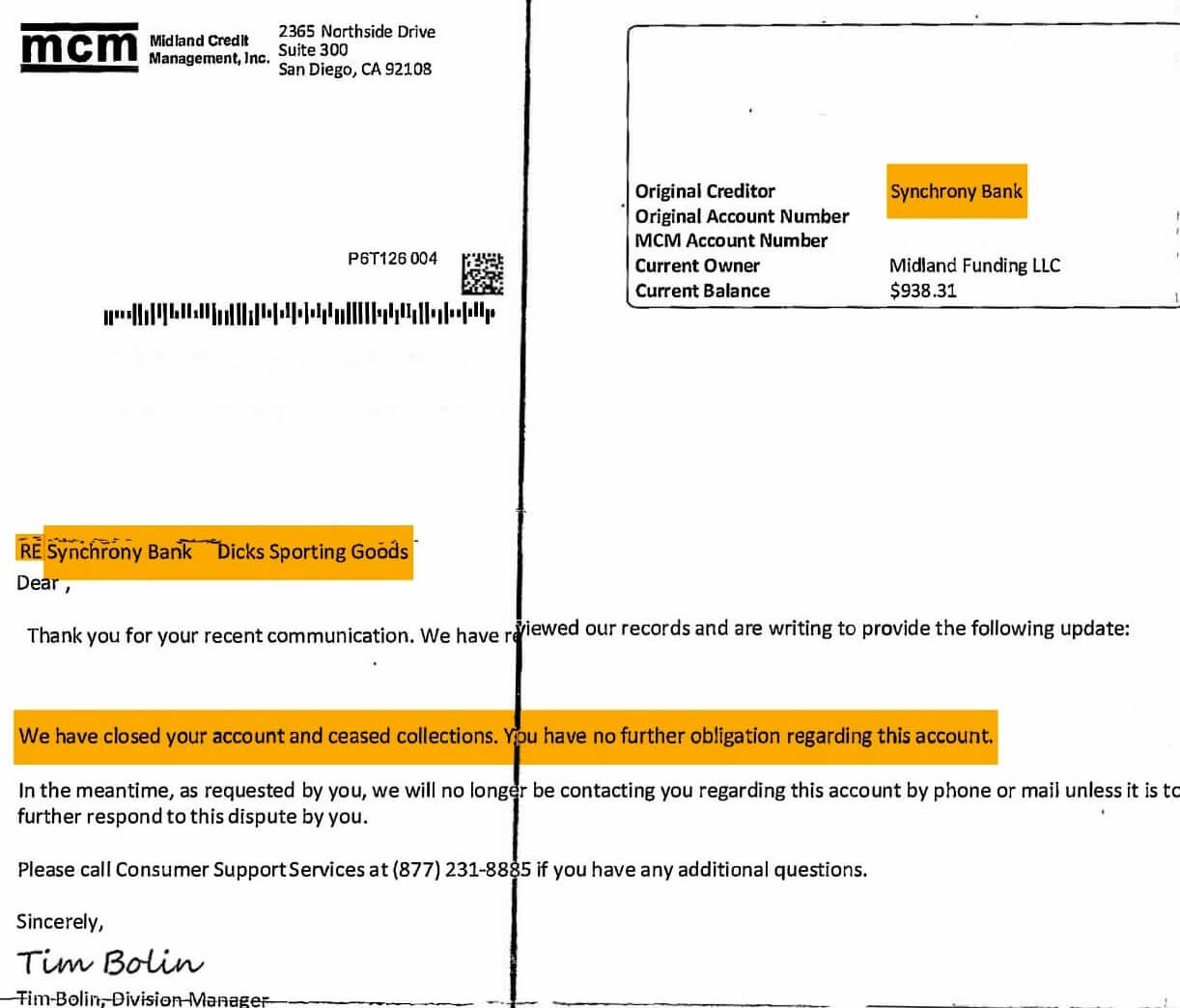

At that point, if the collector continues to try to collect on the invalidated debt, you can sue them. However, rather than getting sued, collection agencies quickly decide to discontinue collection, as shown here:

The New York Times recently reported, “Billions of dollars in student loans may be wiped out for tens of thousands of borrowers in the U.S. because a lender didn’t keep track of the paperwork verifying ownership of the loans.”

Similar to how if you got a speeding ticket and was genuinely speeding, but yet a lawyer could get the ticket dismissed.

The same concept gets used with debt validation. For example, you may have owned the credit card at one point and used it to purchase items. Still, if the collection agency can’t produce the legal documentation and accurate material legally obligated to maintain and produce upon being requested through a validation program, the debt becomes invalid.

This program is truly one of the most effective options to deal with credit card debt due to the corrupt nature of collection agencies.

But don’t I have an obligation to keep paying every month?

If you want to and you are able, you can. First, however, keep in mind how the debt collection process works – the original creditors get their money either way.

If your accounts are already in collections:

This means that a company that you never signed a contract with, never agreed to do business with, is trying to get money from you. Whenever asked, they are legally required to provide certain proof of their right to collect from you – and they don’t have it.

The people you agreed to do business with (your original creditor–the credit card company) have already received reimbursement for the debt by their insurance and through tax credits and refunds. They made an additional profit when selling the account to the collection agency.

You couldn’t even pay the original creditor if you wanted to.

If your accounts are still with the original creditor (for example, a bank):

You should know that they have insurance on the account, and you’ve been paying for it.

Part of every payment you make goes to their insurance.

If you pay for car insurance every month and someone hits you, you file a claim.

Well, in this case, you’ve been hit by circumstances you didn’t know were coming.

If you let your accounts go delinquent, the bank will still get their money.

In some cases, it will come from the insurance that you were already paying for them.

Many people feel they still ought to keep making their scheduled payments, come what may, even if their current situation is entirely unsustainable.

However, the federal government has consumer protection laws to protect people from having to keep struggling.

Why not use them and know that you did all you could?

Make it your New Year’s Resolution to achieve financial freedom.

Golden Financial Services has opened a nationwide debt relief helpline for consumers to call.

What happens when you call Golden Financial Services for help with credit card debt?

- You can talk with an IAPDA certified counselor for free and learn your debt relief options.

- We can pull your credit report for free and quickly go over which options are best suited for you.

- If you are eligible for a debt relief program, our expert counselors will work hard to get you approved and make the entire process easy.

- Trusted Company Reviews accredit golden Financial Services, IAPDA certified, and Better Business Bureau A+ rated.

If you have past-due monthly payments, you may be interested in this next post about the statute of limitations on credit card debt.