Can’t afford to pay your credit cards, student loans, or debt collection accounts? See Post COVID-19 Related Debt Relief Tips

Student loan and credit card payments have been paused nationwide due to Coronavirus-related debt relief, but monthly payments are about to resume. The following blog post will go over debt relief options and tips so that you know what to do if third-party collection agencies, credit card companies, or student loan lenders demand payments that you can’t afford to pay. You do have options, and federal consumer protection laws are already in existence that can help you resolve your debt problems.

If you’re on the urge of falling behind on credit card or student loan payments or are already delinquent, tips for dealing with debt and credit problems are about to be explained. The fact is, you may not have to pay the debt.

To reiterate the past:

CARES Act & Federal Debt Relief Options

The CARES Act paused federal student loan payments until December 31st, 2020, with zero percent interest. This was a fantastic option for students to utilize, thanks to Donald Trump’s administration. This student loan debt relief has benefited millions of students, allowing consumers to put money away in savings and use the extra funds to pay other debt down. Unfortunately, now that payments are about to resume, the same people that benefited from this relief could now have a hefty price to pay.

Federal Credit Card Debt Relief and Debt Assistance Programs for Debt Collection Accounts – Do They Exist?

The CARES Act did not cover credit card relief, but credit card payments have been paused by most creditors, just not “interest-free.” My advice from day one was: “I don’t recommend consumers defer credit card payments if they can avoid doing so. Credit card deferrals result in the interest getting capitalized, making the debt even bigger. You’ll have to pay that capitalized amount back at some point. That means credit card balances will only be more difficult to pay down in the end, and consumer bankruptcies could potentially skyrocket over the next year.”

Check out the 10 Best Ways to Quickly Clear High Credit Card Balances by Visiting This Page Next

Check out Trump’s Debt Relief Options

Get a Free Consultation from one of Our IAPDA certified counselors at (866) 376-9846. Or, start with an online quote. You can quickly find out what programs are available and whether or not you qualify. You must owe $10,000 or more in unsecured debt to qualify for any debt relief program. Golden Financial Services (GFS) is known for offering the best debt relief services on the market and providing the lowest possible monthly payments. GFS was rated #1 on Trusted Company Reviews for the Top 10 Debt Relief Companies of 2020 and has maintained an A+Better Business Bureau rating since 2004.

GFS counselors are recognized as some of the top financial experts online and have great reputations. Just Google their management team: Wesley Hendrickson, Rick Sorrentino, Concepcion Gutierez, Celina Llanos, and Paul Paquin, to name a few. Consumers can choose from the best debt relief programs on the market through GFS.

Student Loan Debt Relief Options – Post-COVID-19 – (as payments resume)

You can consolidate federal student loans so that you only have one low monthly payment to worry about. Your monthly payment can be as low as zero dollars per month, through income-driven repayment plans, including Pay As You Earn and Income-Based Repayment. Eventually, you’ll be able to apply for loan forgiveness. Every year these plans must get recertified. If you have a public service job, as teachers and police officers do, you can apply for loan forgiveness in as quickly as ten years and for everyone else, 20-35 years.

How the CARES Act Helped with Federal Student Loans

If you’re already on an income-based repayment plan, COVID-19 Student Loan Relief (i.e., The CARES Act) Resulted in:

- 1. annual recertifications getting pushed out one year (e.g., if your recertification was due on March 15th, 2020, it’s been pushed out to March 15th, 2021)

- 2. no payment or interest up until 12/31/2020 (payments will resume in January if you do nothing)

- 3. even though there are no payments up until 12/31/2020 if you’re on an income-based repayment plan, the payments you would have been making during this time are still getting attributed towards your loan forgiveness (e.g., if you’re on the PSLF plan, these past six months of paused payments are still getting attributed towards the requirement of making ten years worth of “qualified payments” to be eligible for loan forgiveness)

This is all great news, but it’s about to end.

What to Do About Student Loan Payments That Are About to Resume in January, if Your Income Was Reduced?

If you’re on an income-based repayment plan already, but your income has been reduced further due to COVID-19, request for your payment to get recalculated. You may want to request an additional 90-days forbearance in the meantime due to financial hardship so that you have sufficient time to switch plans. You can do everything through https://studentaid.gov/. Just log in and request your income-based payment to get recalculated. The larger your family size and lower your income, the lower your monthly payment will be.

If you have not consolidated your student loans yet, start by consolidating. GFS can assist you with consolidating your student loans and getting on an affordable payment plan. Start by visiting the student loan relief online application here.

Or give us a call.

Step by Step Student Loan Relief, Consolidation and Loan Forgiveness (Post COVID-19)

If you’d prefer to consolidate and get on an income-driven plan on your own, here are step by step instructions on how to consolidate and get loan forgiveness.

How much does student loan debt assistance cost through Golden Financial Services?

Our counselors can assist you with student loan relief, making the entire process easy for you. There is a fee for the service, but not due up-front. The total fee for consolidation is under $700, due only after student loans are consolidated and paid in full, and the client is approved for the quoted income-based repayment plan. This includes helping you consolidate and get on the appropriate repayment plan that you select. Student loan monthly payments can be as low as zero dollars per month. The program stays with clients until they eventually are eligible for loan forgiveness. We do all the legwork for you and take over-communicating with your loan servicers on your behalf.

Credit Card Debt Relief Options – Post COVID-19

Contact your credit card company directly if you can’t afford the monthly payment.

Request that they reduce or pause your monthly payment interest-free.

According to Golden Financial Services, “the best option to do on your own to pay off debt, save money, and avoid hurting your credit, is to use the debt snowball method.” Before using the snowball method, you’ll need to start with creating your budget. Here are two free tools to help you out:

Still can’t afford your payments?

Talk to an IAPDA certified debt counselor at Golden Financial Services for free. Debt relief programs can help, but they all include potential downsides. And no debt relief program is guaranteed to be a successful solution.

Consumer credit counseling

Consumer credit counseling programs reduce credit card interest rates and offer you a route to pay a single monthly payment for all cards. Not all creditors will agree to consumer credit counseling plans.

The good:

- debt free in just under five years paying less interest

- late payments can be re-aged to show current again

- a single payment for all cards

The bad:

- more expensive than settlement

- not all creditors agree to reduce interest rates, especially post-COVID-19

- only credit cards qualify

- the negative effect occurs at the end of the program when credit card accounts get closed

WARNING: Many consumer credit counseling companies across the nation are turning to debt settlement businesses because many creditors are not willing to reduce the interest rate. So if you contact a consumer credit counseling company, be careful that they don’t redirect you to debt settlement without being fully transparent about it. Make sure you understand the differences between consolidation, settlement, and validation.

Debt Settlement Programs

Debt settlement negotiators can work out a deal where you end up paying only a fraction of what you owe. You will only have to pay a single payment every month. This payment will be lower than what you’d be paying when paying minimum payments on your own. The downside with debt settlement is that you’ll end up with late and collection accounts on credit reports.

The good:

- debt-free in around four years or less

- one payment every month

- pay less than the total owed

The bad:

- most negative affect on credit

- the potential of getting sued and tax consequences

- not all creditors will settle, and not all clients make it through the program successfully

- only one account at a time is negotiated

WARNING: Check a company’s reviews online. If you find hundreds of complaints, that’s an obvious red light, so stop and reconsider. If you question a debt settlement company about their complaints or government action and they respond saying, “these complaints are fake,” or “due to the size of our company, this is a small number of complaints,” that’s another big red flag.

Debt Validation Programs

Debt validation could be your least expensive route to dealing with high unsecured debt collection accounts. The debts don’t get paid but instead are disputed by using consumer protection laws. After an account gets invalidated, it can no longer legally remain on credit reports and does not have to get paid. Worst case scenario, if an account is validated, you can then always use debt settlement as a last case scenario.

The good:

- least expensive and fastest route

- almost all unsecured debt qualifies

- comes with a money-back guarantee and credit restoration

- no tax consequences on invalidated accounts

- all debts are disputed immediately after accounts are in collection status (with settlement programs, only one debt at a time is addressed)

- after accounts get invalidated, the debts and associated negative marks can no longer legally remain on credit reports

The bad:

- like with a settlement program, there’s the potential of getting sued

- creditors don’t get paid, so there will be an adverse effect on credit reports over the first year of the program

- not all clients will make it through the program for various reasons, including their inability to be able to afford all of the monthly payments

For the pros and cons of each debt relief program and disclosures, visit this page next.

Debt relief program downsides and how to deal with them

Debt relief programs come with downsides, but as long as these downsides get addressed, they should not prevent clients from being successful with the plans. For example: With a debt validation program, if a client is issued a summons to go to court over a debt while on the plan, they get a full refund on that account and referred to a settlement law firm to assist the client in settling and resolving the debt for less than the total owed. The account will then be able to get paid off and satisfied for less than the full amount, using the refund to fund the settlement. So, in the end, all debts are fully resolved, and clients still end up saving money.

Similarly, if a client receives a credit card summons while enrolled in a debt settlement program, that summons can easily get settled and resolved before the court date. The client needs to be prepared and warned about this potential downside up-front. People need to understand that when using debt settlement and validation programs, there is a chance that creditors will pursue legal remedies to collect on a debt. People also need to understand the plan of action to resolve the debt if they are served on a summons. At GFS, we take the downsides seriously. The programs that we offer are transparent about potential downsides and have proven methods to deal with downsides if they occur. Please don’t take my word for it; check Golden Financial reviews online and at the BBB.

Most debt relief company complaints occur because:

- companies fail to fulfill their contracts with clients

- due to clients not being fully explained the pros and cons of each program

- high-pressured salespeople sell consumers the wrong program

- lack of appropriate customer service department to answer clients’ concerns and update clients regularly

File bankruptcy for credit card debt

Bankruptcy for credit card debt is almost always unnecessary because you have debt relief programs to help you before filing for BK. Debt settlement is a better option to help you pay off credit card balances over having to file for BK over credit card debt. Bankruptcy can be beneficial if used to save your home from foreclosure and if you’ve already been sued on multiple credit cards. There are times where bankruptcy may be a person’s best route. Chapter 7 Bankruptcy did make GFS’s list for the Top 10 Ways to Clear High Credit Card Debt Quickly.

Debt Assistance Programs

Debt assistance programs include consumer credit counseling, debt settlement, and debt validation programs. Compare the pros and cons of each program by visiting this page next.

How to protect yourself from financial scams related to Coronavirus

Debt relief companies are regulated by the FTC, Attorney General, BBB, and state officials. Most states require companies to be licensed for debt management and credit counseling. Check if a debt management company is licensed, has positive online reviews, and has a high BBB rating before doing business with them.

Debt settlement companies can’t charge up-front fees before results are obtained. If you join a credit card debt settlement program, the company can only charge you a fee after your debt is settled, and at least one payment has been made towards that settlement. Make sure the company explains that you could get sued, and if that happens, how will they help you resolve it? Understand that for debt settlement to be successful, accounts must first go to third-party debt collection status, and collection accounts can make it very difficult to restore your credit score.

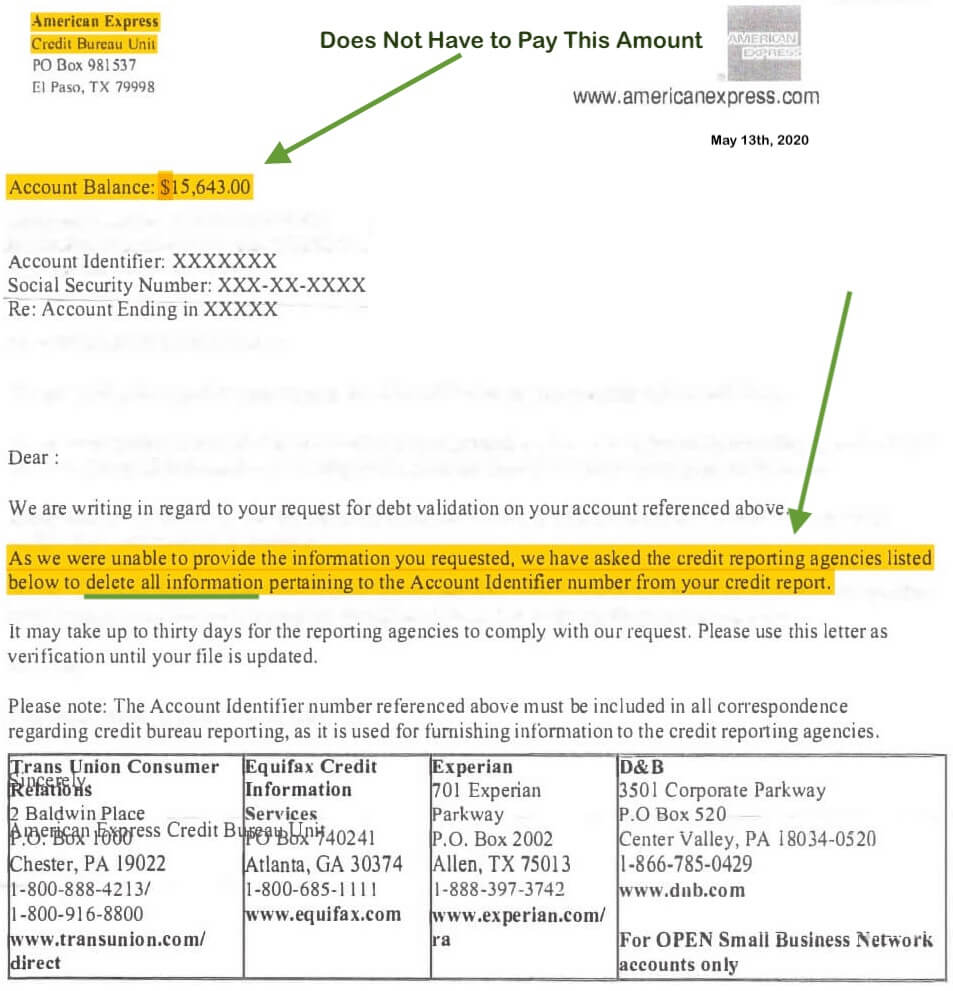

Before settling credit card bills, consider a validation program, a less expensive and a more effective resolution. Take a look at this next example; over $15,000 in credit card debt resolved through debt validation. This is a common result.

How to Deal With Debt Collectors and Consumer Protection Laws

If the last time you made a payment on a credit card debt was over 4-7 years ago, the debt could be expired past the statute of limitations. The statute of limitations varies from state to state. For example, in California, the Statute of Limitations on a credit card debt is only four years. The Statute of Limitations for credit card debt in the state of New York is six years. So this number varies from state to state. See what the Statute of Limitations is in your state by visiting this page next.

Consumer Protection Laws Include:

- Fair Debt Collection Practices Act

- Fair Credit Billing Act

- Fair Credit Reporting Act

- Statute of Limitations

- Credit Card Act of 2009

If you owe above $10,000 in combined credit cards, medical bills, and unsecured loans (including third-party collection accounts), you could qualify for a debt validation program to help you deal with these debts. After accounts are invalidated, legally, collection agencies can no longer report the accounts on credit reports. All collection activity must stop after accounts get disputed until the collection agencies can prove that they are legally authorized to be collecting on the debt, that the amount they claim you owe is accurate, and that they are “licensed debt collectors” in the state that you reside.

What may seem like a huge credit card debt may actually be a lot easier to resolve than you think! For more information on debt validation and to see example letters and cases, visit this page next.

COVID-19 Debt Consolidation Loans and Grants

We saved consolidation and grants for the last items to discuss. These can be your two most expensive routes. Why would you want a loan to pay off debt? The only valid reasons to use a loan to pay off debt include because:

- you want to maintain a high credit score

- you want to avoid having to fall behind on payments

- you want to be able to replace multiple payments with one consolidated loan

- you want to save money in interest

The problem is that:

Lenders are making it very difficult to qualify for a debt consolidation loan Post COVID-19. Banks are afraid consumers won’t be able to pay the loan back due to reduced incomes, so they’ve tightened up their lending policies post-COVID-19. As a result, fintech online lenders are opening up everywhere. These lenders offer loans with high fees and interest rates. These lenders may at times secure the loan with your home or even your car and are extremely high-risk loans. Be careful!

If you do want to apply for a consolidation loan, start here. Our system has been linked up with over one hundred reputable lenders to make it easier for consumers to compare loan options and quickly find out if they qualify or not. These lenders are all offering debt consolidation loans for consumers that have had their income reduced due to COVID-19. Interest rates may vary with each lender so make sure to carefully examine the fees and interest rates associated with any loan before agreeing to one. Read the small print carefully! If you find out you don’t qualify for a loan, visit Golden Financial Services and apply for a debt relief program. COVID-19 debt relief has been implemented into our programs, offering consumers extra savings and lower monthly payments available for the remainder of 2020.