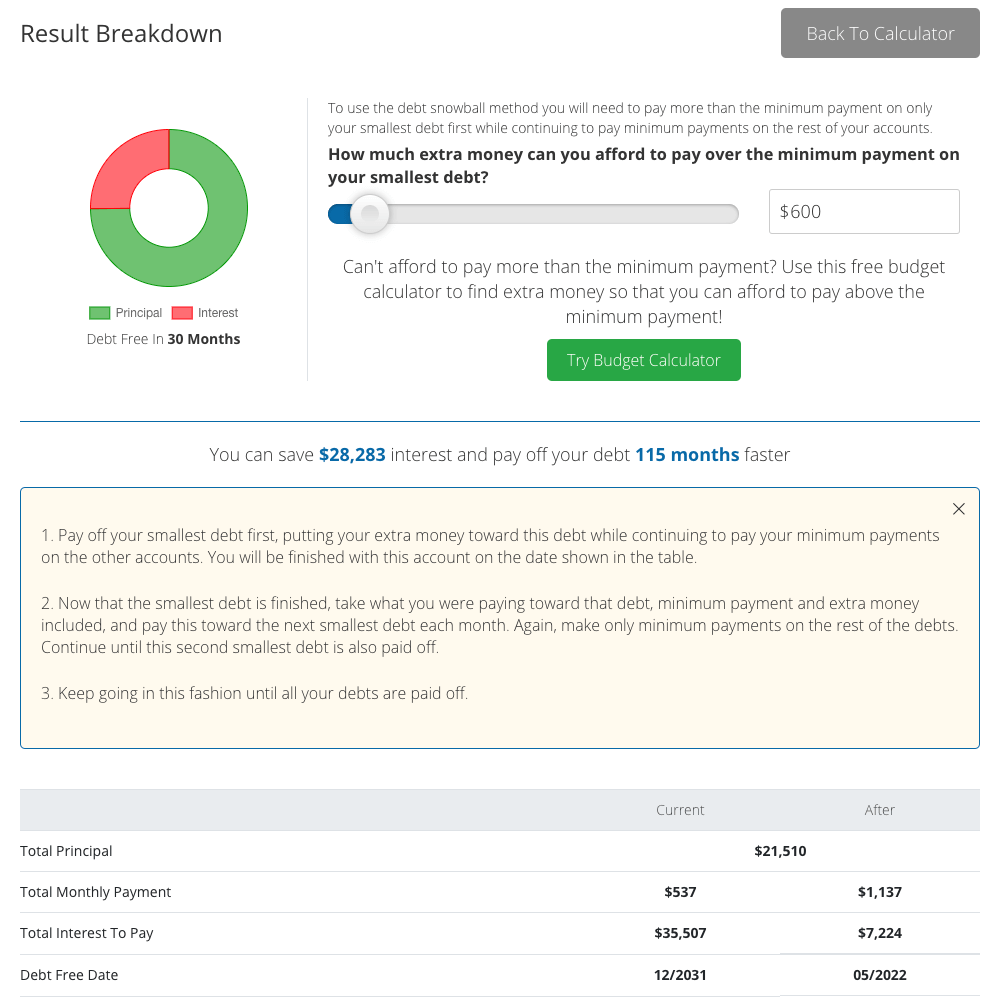

To use the debt snowball method you will need to pay more than the minimum payment on only your smallest debt first while continuing to pay minimum payments on the rest of your accounts.

Can't afford to pay more than the minimum payment? Use this free budget calculator to find extra money so that you can afford to pay above the minimum payment!

Try Budget CalculatorYou still have $ remaining in your wallet. You can now use this extra money (or a portion of it) to quickly pay off your debts with the debt snowball method!

Pay $ Extra Per Month1. Pay off your smallest debt first, putting your extra money toward this debt while continuing to pay your minimum payments on the other accounts. You will be finished with this account on the date shown in the table.

2. Now that the smallest debt is finished, take what you were paying toward that debt, minimum payment and extra money included, and pay this toward the next smallest debt each month. Again, make only minimum payments on the rest of the debts. Continue until this second smallest debt is also paid off.

3. Keep going in this fashion until all your debts are paid off.

| Current | After | |

|---|---|---|

| Total Principal | $ | |

| Total Monthly Payment | $ | $ |

| Total Interest To Pay | $ | $ |

| Debt Free Date | ||

Welcome to the Golden Financial Services Free Debt Snowball Calculator Tool! The debt snowball method is the fastest way to pay off debt while simultaneously improving credit scores.

There are many explanations online about the snowball method, but one of my favorites is one that I stumbled across on TikTok.

@meet.jaz I wish someone taught me this when I was in credit card debt 😒😫 #creditcard #debtfree #savemoney #wealthy #mindset #lgbtq #loveislove #lesbian #gay ♬ Low Volume At 4 AM – Lofi Instrumental Beats Kingz

Debt Ramsey’s debt snowball method is one of the fastest ways to become debt-free (outside of a debt relief program), but how do you calculate the math? Debt snowball spreadsheets are available to help you formulate your debt repayment plan and handle the math aspect of it, but unless you’re advanced in using excel, spreadsheets are not the best tool to use. The debt snowball calculator above is free and much easier to use than a debt snowball spreadsheet. Just enter the details of your budget and creditors, and let the calculator do the rest.

Why is Golden Financial Services giving away this valuable tool for free?

Our corporate mission is to “help people live their lives without debt.” Whether you qualify for a program or not, we still want to be able to help. Not everybody will be eligible for a program, or in some cases, a person may not want to use a debt relief program because they’re concerned about the adverse effect it has on their credit. With the snowball method, credit scores improve as balances get paid down, due to your credit utilization ratio improving.

Do you have an Android device? Try the Debt Snowball App, a free debt payoff planner made for Android.

What if I can’t afford to snowball?

If you find out that you can’t afford the debt snowball method, at that point you may want to explore debt relief programs. Simply give one of our IAPDA certified counselors a call at (866) 376-9846. There are multiple programs available as of 2020 and you can enroll in the plan of your choice with ease.

Golden Financial Services defines the “debt snowball method” as the following:

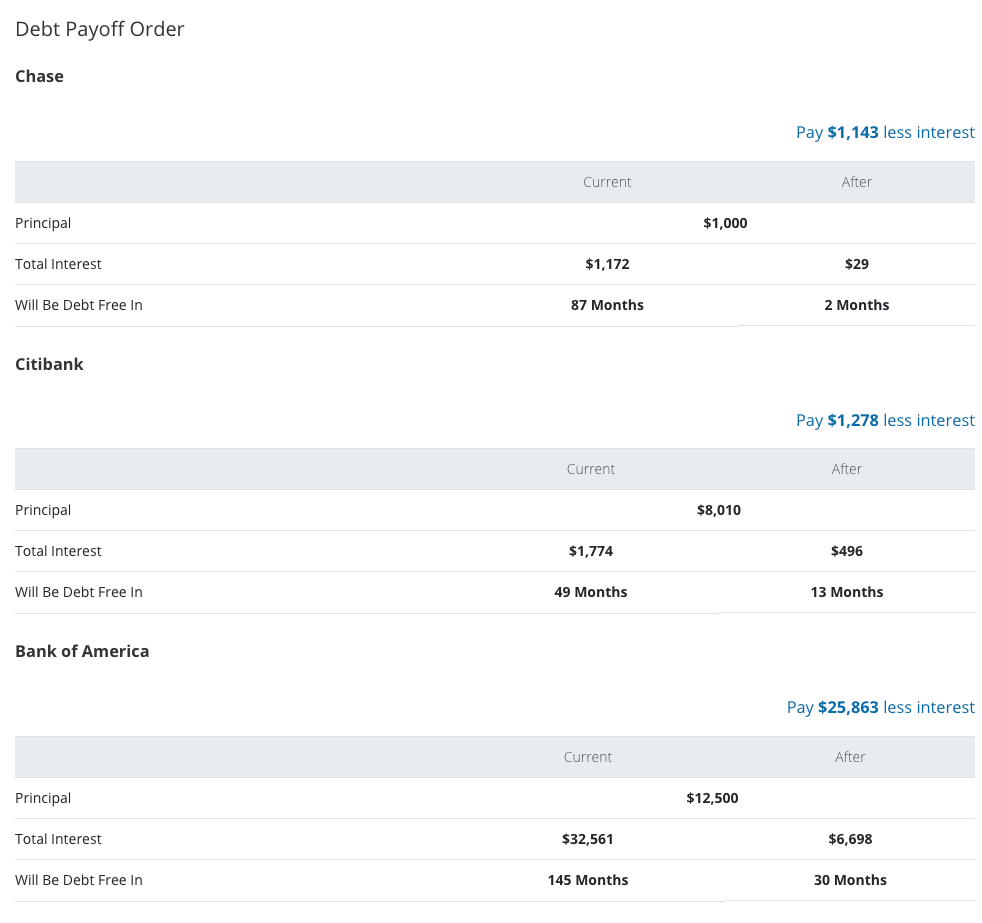

The debt snowball method is a debt reduction strategy, whereby a person organizes their debts from small to large. The objective is to always focus on paying off the smallest balance because that’s the fastest path to getting results. The snowball method uses psychological principles to motivate an individual to keep going until they’re debt-free. These psychological principles are related to dopamine. After successfully achieving the goal of paying off that smallest debt, a person’s brain releases dopamine. They feel good and their brain wants more so that feeling is what drives them towards paying off the next account in line. After paying off the smallest debt, shift the focus to the next smallest debt in line. One by one, just like the effect of dominos, each debt will get paid in full. A person continues in this pattern until they’re debt-free. The snowball method prioritizes debt from small to large because the smallest accounts are the ones that get paid off in the quickest time frame. People often lose their desire to accomplish a goal because they don’t see results fast enough. For that reason, the snowball method focuses on getting results quickly. You get results quickly by going after the easy win (i.e., paying off your smallest balance first). A requirement of the snowball method is to pay more than the minimum payment towards the smallest account every month until it’s paid in full, while simultaneously paying minimum payments on all of the other accounts. Part of the snowball method is finding additional cash flow to be able to afford to pay more than the minimum payment on one account at a time. A person finds extra cash flow by making a budget analysis prior to starting the debt snowball method. The visual created by the budget analysis is what makes it easier to find ways to reduce or eliminate expenses, resulting in more cash flow that will be used towards paying off debt.

Our free budget and snowball calculator tool does all of the work for you. Start with the budget analysis.

You’ll need to enter all of your expenses, which could possibly be exported from your bank account to ensure nothing gets missed.

You’ll then get directed to the snowball calculator above, where you’ll need to enter all of your debts that you want to pay off.

This tool makes the entire process easy to figure out and “dummy-proof”.

As you can see, this tool is super easy to use. Use the slider above to play with your savings based on how much you can afford to pay above the minimum payment. If you believe you can’t afford to pay anything above the minimum payment, think again and try using this budget calculator!

If you truly can’t afford to pay your credit card debt, consider a debt relief program. You can choose from multiple plans; debt settlement, consumer credit counseling, and debt validation. Click here to compare your savings on each program by using this debt relief program calculator.

To check debt relief program eligibility call (866) 376-9846.

Steps to use it:

This free debt snowball calculator tool is super easy to use, does not require you to link your bank account or credit card accounts, and there is no sign up required! The snowball calculator is one of the most effective tools online to help consumers quickly pay off debt.

Academic studies have proven the debt snowball method to be the quickest way to pay off credit card debt and improve credit scores. Psychological principles guide the methodology behind the snowball method, using the brain’s dopamine as it’s number one source of fuel to push the throttle and motivate a person to continue working towards becoming debt-free. In short, it’s the fastest path to getting your first debt paid in full, which will then accelerate you to paying off the second, third, and eventually becoming debt-free.

After paying off your first debt, the dopamine in your brain kicks in, telling you, “Wow, that feels good, it worked! Let’s pay off another debt now!” Not only that, but each time you pay off debt, more and more momentum builds up, and you have a more significant chunk of available cash-flow (similar to how a snowball builds in size as you roll it) to aim at paying off the next debt in line.

A step in advance of the debt snowball method is to use the budget calculator here. By making a budget analysis before using the debt snowball calculator, you will be able to see all of your expenses easily. Why is this important? To use the snowball method, you need to find extra money. To find the extra money, you need to see all of your expenses. You can then scroll down and find ways to reduce your expenses, increasing your available cash-flow. As you grow your available cash-flow, you can use that money to put towards paying off your smallest debt.

You can quickly go back and forth between the snowball and budget calculator to make adjustments, and results will show in real-time.

The debt avalanche method is when you focus on paying off your account with the highest interest rate first. If you do have the mental willpower to tough it out and make it to the finish line using the debt avalanche method, then you will likely end up saving more than if you used the snowball route.

The debt snowball and avalanche method are both great methods to use to pay off your bills quickly. Figure out which route you want to take, fully educate yourself on the process of how it works, and then stick to it!

Consolidating your debt with a loan typically has a five year payoff period at a fixed rate. If you can get a loan with an interest rate of 18%-20%, the monthly payments would be approximately $570-$580, or about $6–$7 a month more than the snowball route.

However, the debt would be paid off in five fewer months at a total cost of around $34,000.

That means a savings of more than $1,900.

A debt management program (also known as consumer credit counseling) works when credit counselors work with your credit card companies to reduce the interest rate on each credit card and arrange a monthly payment schedule the consumer can afford. There also is a monthly fee involved in debt management plans that can be up to $50 per month.

The projected interest rate reductions for this example were 8% for card #1; 12% for card #2; 10% for card #3 and 8% for card #4. As one card gets paid off, that money is allocated to the card with the highest APR.

The monthly payment, including fees, would be $514 a month, and the debt would be eliminated in just under five years by using consumer credit counseling.

Where you use consumer credit counseling or the debt snowball method, don’t delay getting started today!