Whether you live in Little Rock, Bentonville, Hot Springs, Fort Smith, or Fayetteville, Arkansas, debt consolidation programs can help you escape high unsecured loans, medical bills, collection accounts, and credit card debt.

Credit card debt relief programs, including consumer credit counseling in Arkansas, are another route to help consumers reduce credit card interest rates and consolidate Debt.

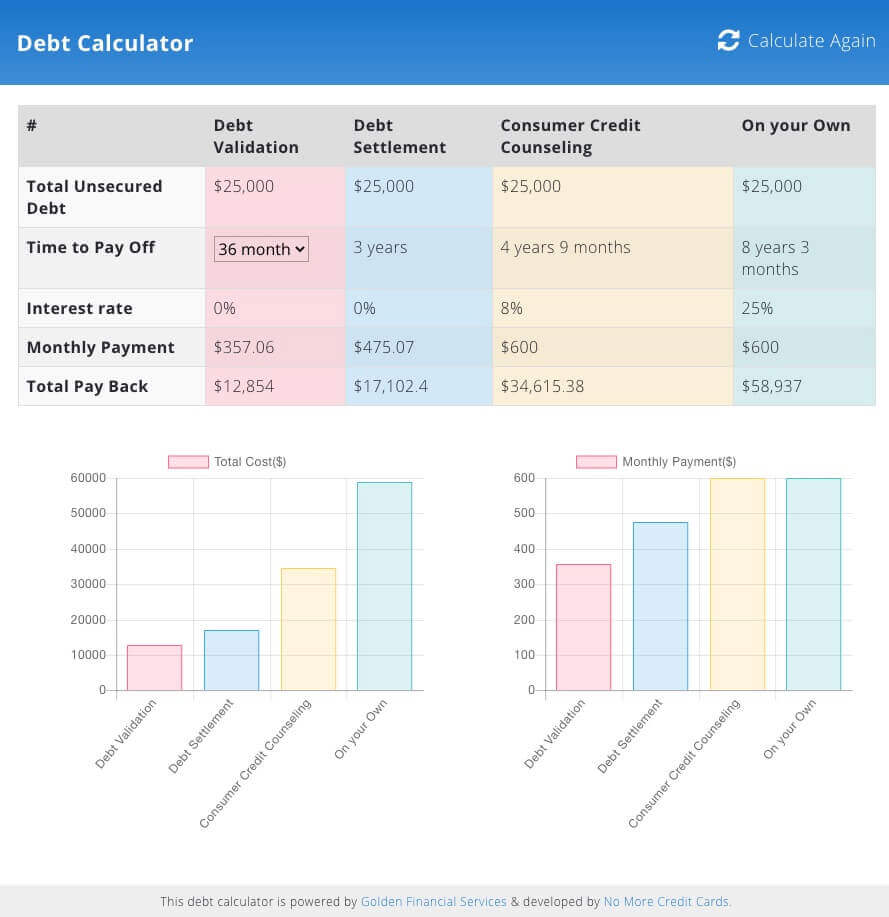

The following page should be viewed for informational purposes only, and GoldenFs.org, including Golden Financial Services, does not offer any debt help or services.

Table of Contents

- Overview of Arkansas Debt Consolidation Options

- Consumer Credit Counseling in Arkansas

- Debt Consolidation Loans for Arkansas Residents

- Government Resources for Debt Assistance

- Arkansas Debt Relief Laws and Protections

- Tips for Managing Debt in Arkansas

- Credit Counseling Fees and Disclosures

Overview of Arkansas Debt Consolidation Options

Debt consolidation and consumer credit counseling are two of the most effective ways for Arkansas residents to manage and reduce debt. These options provide structured repayment plans that simplify debt management, lower interest rates, and help avoid severe credit impacts.

Benefits of Debt Consolidation:

- Combines multiple payments into one.

- Reduces interest rates, saving money over time.

- Helps avoid missed payments and late fees.

- Offers a structured pathway to becoming debt-free.

Consumer Credit Counseling in Arkansas

What Is Consumer Credit Counseling?

Consumer credit counseling helps individuals manage unsecured debts like credit cards by negotiating lower interest rates and consolidating multiple debts into a single monthly payment. This method is especially useful for individuals with steady income who are struggling with high-interest debt.

Pros:

- Lower Interest Rates: Reduces the overall cost of debt repayment.

- Simplified Payments: Combines multiple payments into one manageable monthly payment.

- Minimal Credit Impact: Payments are made on time, avoiding the severe impact of missed payments.

- Financial Education: Many programs offer budgeting and financial planning resources.

Cons:

- Credit Card Closure: Enrolled accounts are closed, potentially lowering your credit score.

- Program Duration: Plans typically last 4-5 years, requiring consistent payments.

- Credit Notation: Credit reports may show participation in a credit counseling program, which some creditors view negatively.

Who Should Consider Credit Counseling?

Consumer credit counseling is ideal for Arkansas residents who:

- Want to avoid the credit score impact of missed payments.

- Are ready to commit to a structured repayment plan.

- Have steady income but are struggling with high-interest debt.

Debt Consolidation Loans for Arkansas Residents

What Are Debt Consolidation Loans?

Debt consolidation loans allow you to combine multiple debts into one loan, ideally with a lower interest rate. This option is particularly beneficial for individuals with strong credit scores.

Benefits:

- Lower Monthly Payments: Longer repayment terms can reduce monthly obligations.

- Simplified Debt Management: Combines multiple debts into one payment.

- Improved Credit Utilization: Paying off high-interest accounts can boost your credit score over time.

Challenges:

- Qualification Requirements: Applicants with poor credit or high debt-to-income ratios may not qualify.

- Interest Costs: Longer terms may lead to higher total interest paid.

Where to Find Debt Consolidation Loans in Arkansas:

Local credit unions and online lenders often offer competitive rates. Be sure to compare terms, fees, and interest rates to ensure you’re making the best choice.

Government Resources for Debt Assistance

While there are no federal or state debt relief programs specifically for credit card debt, Arkansas residents may benefit from federal student loan consolidation programs and other government resources.

Federal Student Loan Consolidation:

Arkansas residents can consolidate their federal student loans through the Department of Education. Benefits include:

- Income-Driven Repayment Plans: Monthly payments are based on income and family size.

- Loan Forgiveness: Public service workers may qualify for forgiveness after 10 years of service.

- Simplified Payments: All loans are combined into one manageable payment.

Arkansas Debt Relief Laws and Protections

Key Legal Protections:

- Statute of Limitations: In Arkansas, creditors have five years to file a lawsuit for unpaid debts. After this period, debts become legally unenforceable.

- Fee Transparency: Licensed credit counseling organizations must clearly disclose all fees and program details.

- Consumer Protection Laws: Arkansas residents are protected by both state and federal laws regulating debt collection practices.

Tips for Managing Debt in Arkansas

- Create a Budget: Use a budgeting tool to track expenses and identify areas for savings.

- Snowball Method: Focus on paying off the smallest debts first while making minimum payments on larger debts.

- Negotiate with Creditors: Many creditors are willing to lower interest rates or offer payment plans if approached directly.

- Monitor Your Credit: Regularly check your credit report to track progress and ensure accuracy.

Credit Counseling Fees and Disclosures

- Monthly Fees: Consumer credit counseling programs in Arkansas typically charge no more than $50 per month.

- Credit Impact: While credit scores may initially improve due to reduced interest rates and timely payments, closed accounts at the end of the program may lower scores.

- Transparency Requirements: Reputable programs will clearly outline all costs and potential credit impacts.

By understanding your options and leveraging available resources, Arkansas residents can take control of their finances and work toward a debt-free future. Always consult with a licensed financial advisor or credit counseling organization before making significant financial decisions.

Disclosure

Goldenfs.org does not offer any programs or services. This content is intended for informational purposes only. Always consult with a licensed financial advisor or financial professional before making significant financial decisions.

2 comments on “Arkansas Debt Consolidation”

Comments are closed.