How to Negotiate Credit Card Debt Yourself: A Step-by-Step Guide (with Sample Letter)

Managing credit card debt can be challenging, but it’s possible to navigate the process yourself. This guide provides a step-by-step approach to help you communicate with your creditors and potentially improve your financial situation. While every situation is unique, this information can be a valuable resource for those seeking to manage their debt independently.

Understanding Your Options

Before contacting your creditors, it’s important to understand the different approaches you can take.

This includes reviewing your credit card agreements to understand interest rates, fees, and other terms. Understanding your financial situation, including your income and expenses, is also crucial. You may also want to check out our free guide on how to negotiate with creditors.

A Do-It-Yourself Communication Guide

- Review Your Debts: Start by gathering information about all your credit card accounts, including balances, interest rates, and payment due dates. Organize this information so you have a clear picture of your overall debt.

- Assess Your Finances: Create a budget that outlines your income and expenses. This will help you determine how much you can realistically afford to pay towards your credit card debt.

- Contact Your Creditors: Reach out to your credit card companies to discuss your situation. Explain the challenges you are facing and your willingness to work towards a solution. Be prepared to provide documentation of your financial situation, such as income statements or other relevant financial records.

- Explore Options: Inquire about available options, such as lower interest rates, adjusted payment plans, or other arrangements that could make your debt more manageable. Be clear about what you are hoping to achieve.

- Document Everything: Keep detailed records of all communication with your creditors, including dates, times, names of representatives, and any agreements reached. This documentation is essential for tracking your progress and resolving any potential disputes.

- Follow Through: Once you have reached an agreement, ensure you adhere to the terms. Make your payments on time and communicate promptly if any changes in your financial situation arise.

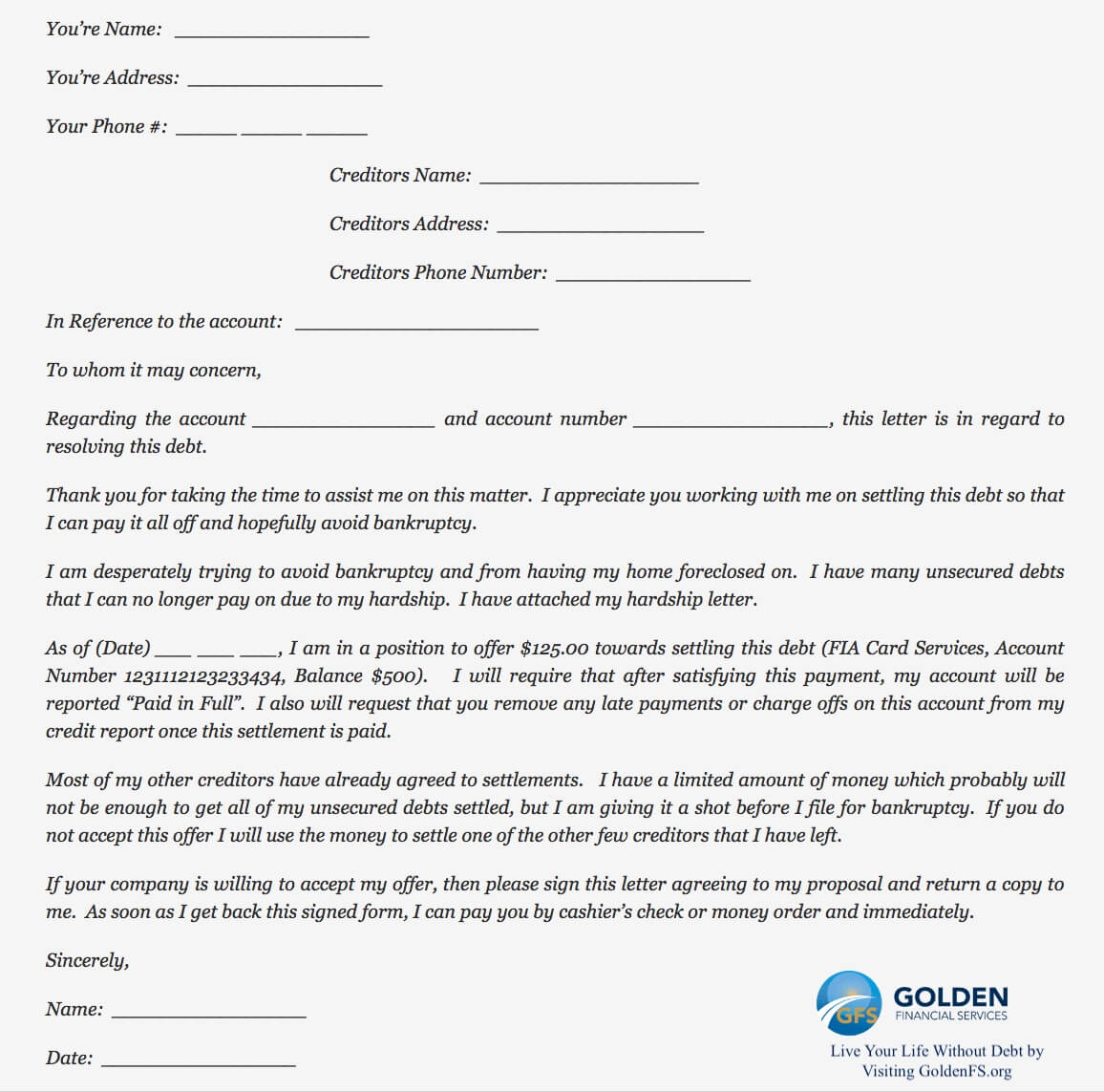

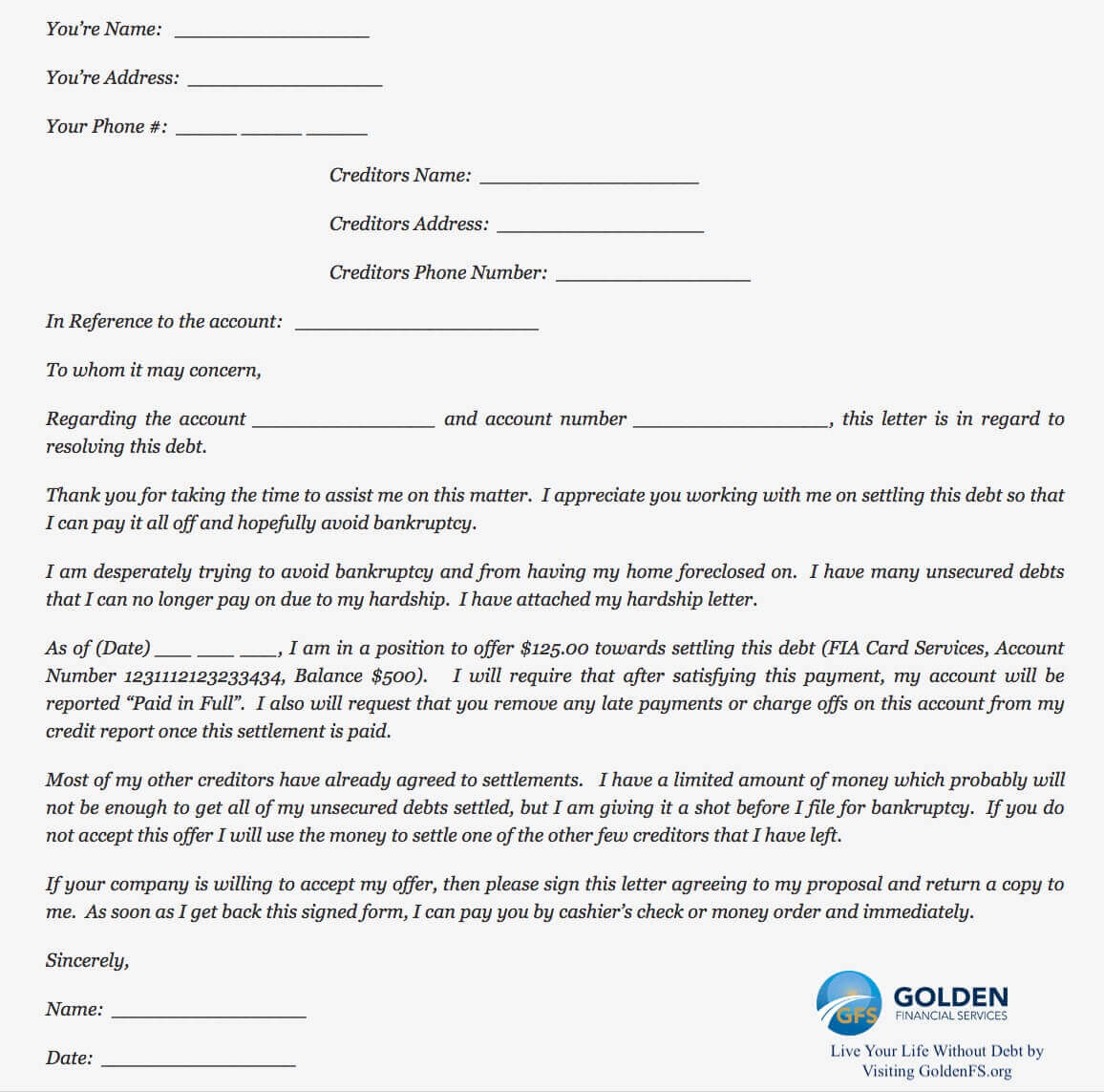

Debt Negotiation Letter Template

Debt Hardship Letter Template (Copy and paste this and then personalize it for your situation)

Your Name

Your Address

Your Phone Number

Debt Collection Company Name

Address

Phone Number

Attention (Supervisor’s Name)

Date:

RE: Settling a (state the type of debt, like a credit card debt or medical bill). Creditor Name and Account Number

Dear (Supervisor’s Name or Creditor Department Name),

My name is (your name). I am currently going through challenging times health-wise and financially, which I’m about to explain.

EXPLAIN YOUR HARDSHIP: I was diagnosed with Lime Disease on (date). I incurred $15,000 in medical debt, and my insurance covered only half. Included with this letter are medical receipts. I stayed at the (include hospital name) on (include dates), and this hospital visit cost (amount) and insurance covered only (amount). This situation has caused me to fall deeper into debt, making it impossible to continue paying on anything besides my mortgage/rent, groceries, etc.… (include a copy of your budget)

I have not been to work in 15 days, and my income has gone from (amount) down to (amount).

I have been on a payment plan with your firm, paying (amount) since (date). Unfortunately, due to this unexpected circumstance in my life, it’s now impossible to continue paying this amount.

This letter includes a settlement offer that I am willing to pay today to resolve this debt in one lump sum payment. The funds that I am eager to offer you today were borrowed from friends and family members who have all contributed all they are willing to provide to help me address my debt.

I’ve also attached my income to illustrate that it’s gone down from (amount per month) to (amount per month). I hope you are willing to work with me to resolve this debt so that I am not forced to file for bankruptcy. I even plan on giving you guys an excellent review online if you can help me out today.

Be sure to get in touch with me as soon as possible to begin the process.

Name

Signature

Date

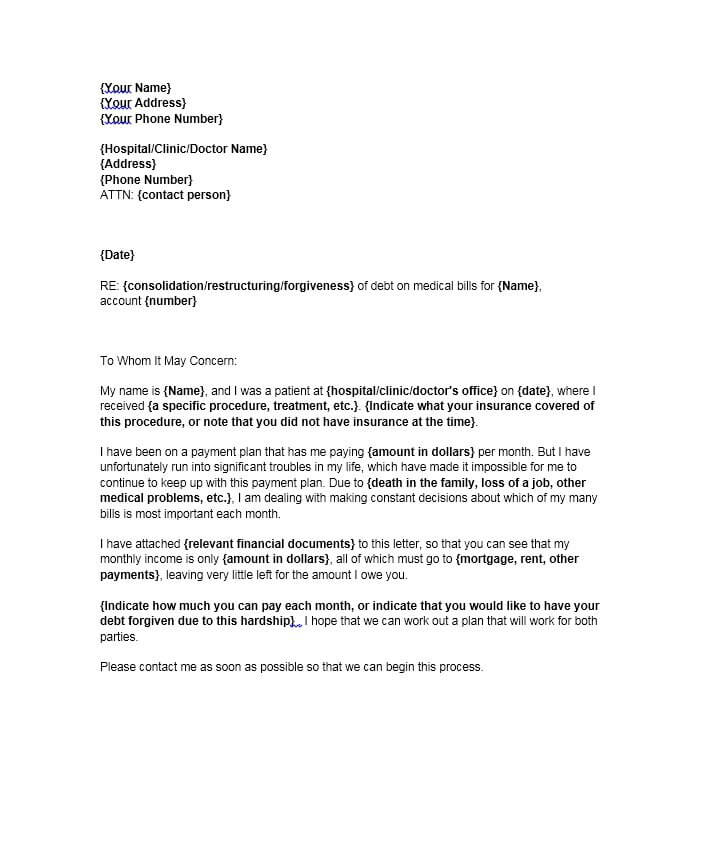

Here’s a 2nd Debt Hardship Letter (specifically for medical debt)

Possibly you like to perform solitary or multi-player mode in, you can use

my gun 3d that is pixel hack on them.

Hi friends, how is the whole thing, and what you desire

to say regarding this paragraph, in my view its really awesome designed for me.

Here is my web blog: top email management agency in Los Angeles CA

I was able to find good info from your blog posts.

I came across your Do it Yourself Debt Settlement – Debt Settlement Letter | GoldenFS.org website and wanted to let you know that we have decided to open our POWERFUL and PRIVATE website traffic system to the public for a limited time! You can sign up for our targeted traffic network with a free trial as we make this offer available again. If you need targeted traffic that is interested in your subject matter or products start your free trial today: http://priscilarodrigues.com.br/url/v Unsubscribe here: http://acortarurl.es/97

Oh my goodness! Incredible article dude!

Many thanks, However I am having troubles with your RSS. I don’t understand the reason why I cannot subscribe to

it. Is there anybody having identical RSS problems?

Anyone who knows the answer will you kindly respond? Thanks!!

Why is it that the creditors must stop calling once notified that I have an attorney? I am contemplating if I should use an attorney debt settlement program or a non-attorney plan. And do you guys offer attorney debt settlement?

What if I prefer to let you guys settle my debt. I have about $32,000 in credit cards. How much would my payment be?

These guys are wonderful. I used their service many years back and was able to resolve over $45K in credit cards. Unfortunately, now I have a Cox Cable debt collection account that appeared on my credit. The balance is only $400 so it’s too small to use the program, but this article will help me settle the debt on my own. Thanks guys so much.

Very great post. I just stumbled upon your blog

and wished to mention that I’ve truly loved browsing your blog

posts. After all I’ll be subscribing for your rss feed and I’m

hoping you write again very soon!