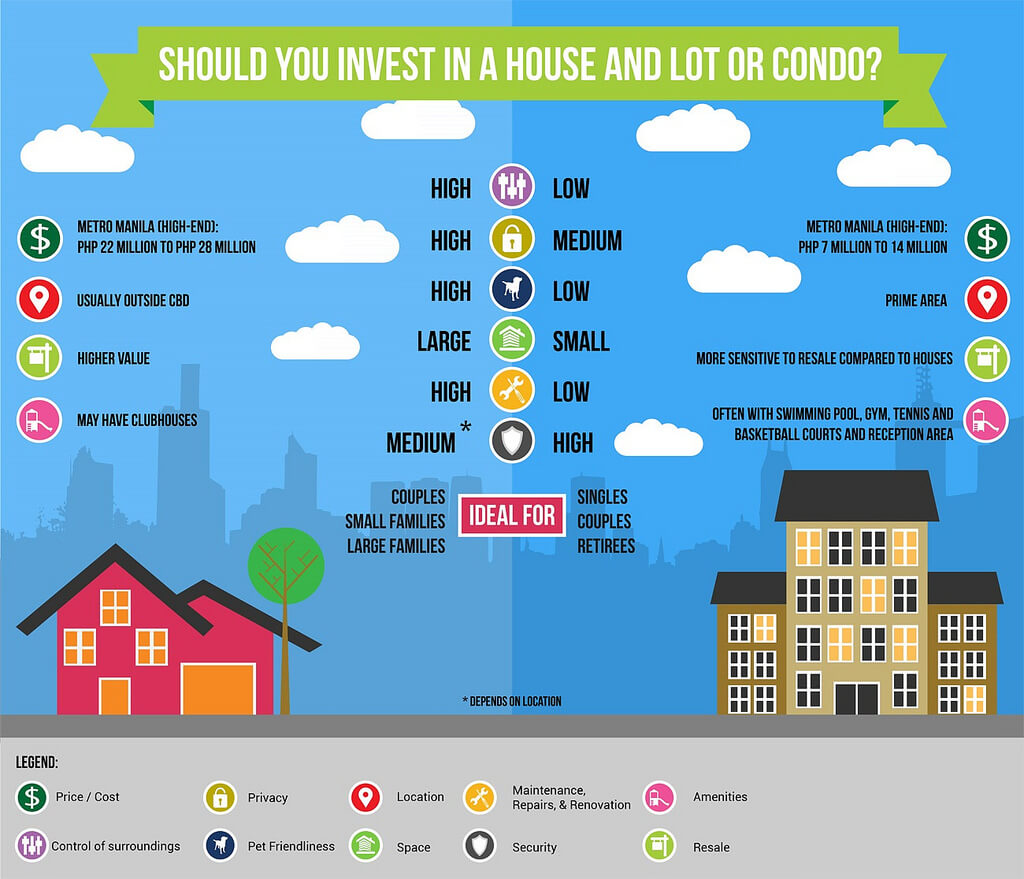

Could you quit your job if you were paid $6,600 or more per month, every month, for the rest of your life? The following blog post will show you how to generate this type of passive income off real estate.

Before getting started, here are a few questions people may have:

What is the minimum requirement of income that you need to make to be able to do this strategy?

Is there a minimum amount that you need to have saved?

The answer is; everyone can benefit from this strategy. In the example below, we show you how to build over $6,600 in passive income from the bottom up. So, depending on how broke or rich you are right now will determine how far into the journey you start.

In the example below the person has $11,000 in savings already and makes around $60,000 per year in annual income. If your situation is better or worse, just adjust the numbers to fit your situation.

The reason we decided to share this information in the first place is that many Golden Financial Services’ clients requested information on how to turn their limited income into passive income. See, Golden Financial Services consolidates debt, making it easier for consumers to pay it off in a quick time-frame. After clients become debt free, the money that they had been paying towards debt every month is now available to use in other ways.

As a result, graduated clients often ask us at Golden Financial Services, “do you know of any good investments that I can participate in, now that I am debt free?” Unfortunately, Golden Financial Services is not a licensed financial advisory firm and cannot provide legal investment advice.

Having said that, the following information will help you understand the concept of real estate investing and how to generate passive income from it. The strategy that I’m about to reveal is one that I learned from the book “Rental Property Investing”, by Brandon Turner.

Without further ado, let’s get started.

Here’s a summary of the real estate investment strategy:

- You will be buying single-family homes and paying only 80% of the assessed value to purchase the properties (meaning, you are only buying “good deals”)

- You will buy one home per year, until year seven, which at that point you will start buying two homes per year (and continue to grow from that point forward)

- Your goal is to generate $6,600 or more in passive monthly income and to be able to quit your job at that point

- Your current income from your regular job is $5,500 per month ($66,000 per year)

- You already have $11,000 in savings that you will use to help jumpstart this real estate strategy

- You will set aside 20% of your income every month for investment purposes ($1,100 per month/$13,200 per year), leaving you with $52,800 per year to live on (every year you will increase the amount you set aside from your personal income that will be used towards your real estate investments)

Year One – simply save $1,100 per month

- Save $1,100 per month from your current personal income, allowing you to save $13,200 by the end of year one. This is the money that you will use to make your first real estate investment. I would recommend that you put this money in a separate bank account, don’t commingle these funds with your regular checking account. You could even open up a one-year bank CD that pays 2%, ensuring your money is only tied up for one year at a time.

- You will add this $13,200 saved at the end of year one, to your initial savings of $11,000, equaling a total of $24,200 to use as your “down payment” on your first real estate purchase.

Year Two – buy your first single family home

- After carefully searching for the right purchase on a property, you finally find a 3-bedroom, 2-bath, 1989 single family home, that is currently a bank foreclosure

- The property has sat on the market for over six months, due to only cosmetic issues on the inside. Fortunately, all it will take for you to beautify this property is a good paint job!

- The home is listed for $110,000. You will offer 80% of the value to buy it (meaning, you will offer the seller $88,000)

- As part of negotiations, you request that the seller pays closing costs (and the seller agrees)

- You’ve successfully purchased this first property for $88,000, congratulations!

- By using the Bigger Pockets rental calculator tool, we figured out that you can earn $330 per month (cash-flow) on this first property. The $330 per month is after paying all expenses, including the $70 that you put aside each month which will go towards paying the taxes on the property at the end of the year, the property management company, vacancy, repairs and capital expenditures.

- You could manage the property on your own and save an additional $100 per month, but that could lead to future headaches. Do you want to be the one having to fix the toilets? Always run your real estate investments like a business, not a personal hobby or even worse “a job”. Delegate certain tasks and think “big picture”.

- You decide to increase your personal savings by an extra $110 per month every year. (save $1,100 per month on year one from your personal income, $1,210 in year two, $1,320 in year three, and so on…)

- You now have $330 per month (cash-flow) from property one’s rental payments, plus the $1,210 from your personal income, equaling a total of $1,540 per month for all of year two.

- By the end of year two, you have a grand total of $18,480 saved, enough to purchase property number two.

Year Three – purchase second rental property

On this second rental property, the scenario will stay the same:

- The property value will be $110,000, but you purchase it for $88,000

- The down payment will be $17,600 (20%)

- You will save $330 (your monthly cash-flow) after all expenses are paid from the rental income on the second property, added to the $330 saved on the first rental property, plus your $1,320 “monthly savings” from your job, equaling a total of $1,980.

- At the end of year three, you have a total of $23,760 that you can use to purchase your third rental property.

Year Four – purchase your third rental property

Again, the figures will stay the same. You will be purchasing a single family home that has a value of $110,000, which you can purchase for $88,000 (80% of the value).

After all of the expenses get paid you’re left with $330 (monthly cash-flow from the rent payments). Add that to the $330 from your first rental property, plus the $330 from your second rental property, plus the $1,430 (personal savings from your job), equaling a total of $2,420. At the end of year four, you now have $29,040 to use for another purchase.

Year Five – purchase your fourth rental property

You now have $29,040 available to purchase your fourth rental property. However, the down payment is only $17,600, so you’ll be left with some extra money that can be used for repairs. As Dave Ramsey preaches, always have an emergency fund in place for life’s unexpected expenses. In the real estate world, property expenses can come out anywhere.

We will use the exact same numbers as used on the other properties, the only difference will be that your personal savings from your job increases.

Years 6-10 – your passive income starts to skyrocket!

By the end of year six, you are saving $1,650 per month from your personal income and $1,650 per month from your five rentals, equaling $39,600 per year. With $39,600 per year in available cash-flow, you can afford to purchase two rental properties. The magical power of “compound interest” starts to skyrocket your savings at this point!

You start to increase the number of properties that you buy after year seven. You can buy two properties in year seven, two properties in year eight, three properties in year nine, four in year ten and five in year eleven.

- In year seven, you will purchase two properties and own seven rentals; your job savings has increased to $1,760 per month, plus your cash-flow of $2,310 from rental income, equaling a total of $48,840 in available funds to use.

- In year eight, purchase two new properties, you already own nine rentals, your job savings has increased to $1,870 per month, plus your cash flow of $2,970 from rental income, equaling a total of $58,080 in available funds to use towards your next investments.

- In year nine, purchase three new rental properties. You already own twelve. Your job savings is now at $1,980 per month, plus your cash flow of $3,960 per month, equaling a total of $71,280 which can be used to purchase your next investments.

- In year ten, you will purchase four rental properties and have sixteen rentals in total, your job savings is now at $2,090 per month, plus $5,280 per month from your rental income (total cash-flow), equaling a total of $88,440 in annual savings.

- In year eleven, you will be able to purchase five rental properties and already own twenty-one rentals in total, your job savings is now at $2,200 per month and saving $6,930 per month from your rental income (total cash-flow), equaling a total of $109,560 in annual savings. You can finally retire at this point, living off the passive income generated from your rental properties. Or, keep going!

At this point in the game, you’ve accomplished your goal of earning above $6,600 per month in passive income.