Are you ready to quickly clear your credit card debt in 2023? The ten best ways to get out of debt are about to be revealed. Clearing credit card debt is never an easy task. However, credit card relief comes to you much easier when using an effective debt solution personalized for your situation.

As of 2023, as interest rates have skyrocketed, everyone should be looking to pay off their credit card bills faster because debt is the most expensive it’s been in the last decade. “Greg McBride, Bankrate’s chief financial analyst, believes the average interest rate will jump to 20.5% in 2023, following the upward arc of the Fed’s climbing rates.” Source: Bankrate.com

That said, the following guide will make it easier for you to clear those high balances. Here are your “10 Best Ways to Clear Credit Card Debt in 2023”.

Golden Financial Services is no longer offering debt relief programs to the public. The information here is being provided purely for informational purposes.

What are the best debt relief, settlement, and consolidation companies for 2023?

- For debt settlement, use a licensed and FTC-compliant company. Firms like Accredited Debt Relief and Beyond Financial fit those criteria. These companies also don’t charge any up-front fees. For more information about Accredited Debt Relief, reviews can be found on its website.

- For consumer credit counseling, consider a non-profit and licensed company. Visit the website for the Department of Justice at: https://www.justice.gov/ust/list-credit-counseling-agencies-approved-pursuant-11-usc-111.

- For debt consolidation lenders, ensure they are licensed and highly rated at the BBB.

Unsecured debt includes:

- Credit cards

- Medical bills

- Unsecured loans and collection accounts

- Paypal credit cards and loans

- Student loans

How can I clear my credit card debt fast? The rest of this blog post provides a more detailed analysis of each option explained above in the info-graphic.

Even the rich and famous have credit card debt. Renowned musician, David Cassidy, had over $300,000 in credit card debt. According to a federal court filing, actor Stephen Baldwin owed over $70,000 in credit cards. When Bernie Sanders and Ted Cruz were required to file financial disclosures for the presidential race many years back, it was revealed that they both owed above $60,000 in credit card debt. So, if you have found yourself struggling to pay off large credit card bills, know – you’re not alone.

Table of Contents

- 1. Debt Snowball Method

- 2. Debt Avalanche

- 3. Balance Transfer Cards

- 4. Home Equity Line of Credit

- 5. How to Negotiate With Bank

- 6. Credit Card Hardship Program with Bank

- 7. Debt Validation

- 8. Debt Settlement

- 9. Consumer Credit Counseling

- 10. Bankruptcy

1. Debt Snowball Method:

The debt snowball method is the best way to get out of credit card debt for anyone who can comfortably pay more than minimum payments.

The debt snowball method, created by Dave Ramsey, is when you pay minimum payments on all of your credit cards besides the one with the smallest balance. Then, you will aggressively attack that smallest debt first by putting all your extra money towards paying it off as fast as possible.

We go after the small debt first to get the quickest result. And fast is the name of the game here. After each debt gets paid in full, your available cash flow will continue to grow, just like when you’re rolling a snowball. Your momentum will also continue to grow as your ball of cash increases in size, and you direct that cash towards paying off the next debt in line.

After the smallest debt gets cleared away, shift your attention to the next smallest debt. You will continue to knock off each debt one by one, getting closer and closer to the finish line.

Start by creating your budget with this free calculator here.

A budget will give you a visual image of where your money is going, making it easier to find non-essential expenses that can be reduced or eliminated. (example: lower the electric and heat bill, use coupons when shopping to save money at the grocery store, remove the HBO you never watch, and cancel that old subscription that you forgot was billing you each month).

You can then use this snowball calculator tool to figure out how long it will take you to become debt-free. Again, the debt snowball calculator does all of the work. Just enter each debt you want to include in the snowball plan, and let the calculator work its magic.

Why Does the Debt Snowball Method Work?

Dave Ramsey explains: “The debt snowball works because it’s all about behavior modification, not math. Hope has more to do with this equation than math ever will when it all boils down. If you start paying on the student loan first because it’s the largest account, it could take years to get rid of that first debt.

Click Here to Use the Budget & Snowball Calculator

One last tip to avoid a big mistake:

Keep your credit card accounts open after paying off the balances to improve your credit score. If you close a credit card account, your credit score will decline because your credit utilization ratio will be negatively affected.

2. The Debt Avalanche

The debt avalanche method is the best way to pay off high-interest credit card debt and reduce your monthly interest fees, according to Andrea Cannon from Wisebread.com.

The debt avalanche method is similar to the debt snowball method, but the difference with the debt avalanche is that you order your debts by their interest rate. So instead of paying off your smallest balance first, you would pay off the credit card balance with the highest interest rate, the one costing you the most.

You can get out of debt faster and maximize your savings by first paying off your most expensive accounts.

You may use a combination of the debt snowball and avalanche methods. For example, start using the snowball method to pay off all your balances under $1,000, then switch to prioritizing your debts by the interest rate and using the debt avalanche method.

NerdWallet.com offers an excellent Debt avalanche calculator tool to help you get out of debt faster.

3. Pay Off Credit Card Debt With a Balance Transfer Card:

“Low Rate Balance Transfers | 0% Intro APR. Apply Now!” Wow, that’s enticing until you read the fine print; “after 12-18 months, the introductory rate comes to an end, and the interest rate rises to 19.9%.” Balance transfer cards also come with up-front fees. These fees range from 3%-5% of the credit card debt getting transferred. If you move $10,000 onto a balance transfer card that charges a 4% fee, that’s $400 in up-front costs.

Banks use balance transfer cards as a trap. They charge you the upfront fee for the card, and when you can’t pay off your entire balance within the introduction-rate period, they jack up the interest rates. They make money when clients fail to pay off the balance within the intro period. They want you to fail.

When is a balance transfer card worth it?

- If you can afford to pay the balance “in full” within the 12-18-month introductory period, you could pay low to no interest and only a $400 fee. Shop around for a low-cost balance transfer card, and only go this route if you can afford to pay the balance in full within the introductory rate period. Use this debt national calculator tool to help you do the math.

- Choose a balance transfer card that pays you cashback. Bank of America offers a credit card that pays up to 3% cashback. For example, if you transfer $50K in credit card debt onto a balance transfer card that pays you 3%, you’ll get reimbursed $1,500 in cashback. Put that $1,500 towards paying off your next credit card debt in line as you continue with the debt snowball method. You can eliminate 100% of interest and earn cashback when using a balance transfer card to pay off high-interest credit card debt.

Final Tip to Improve Your Credit Score

Keep your credit card accounts open after paying off the balances to keep your credit utilization ratio favorable.

4. Home Equity Line of Credit:

You’re taking on considerable risk when using a home equity line of credit to pay off credit card debt. This is because you’re swapping unsecured debt for secured debt. If, for whatever reason, you can’t afford to continue paying your scheduled monthly payments on the home equity line of credit, you could end up losing your home over a credit card debt, wherein you see the risk.

However, this is still one of my favorite tools for clearing credit card debt. The value of using a home equity line of credit to pay off credit card debt is that you’re eliminating high-interest credit cards and replacing them with a low-cost home equity line of credit.

According to Bankrate.com, 5.56% is the average interest rate on a home equity line of credit as of May 2018, significantly lower than the average interest rate on a credit card.

5. How to Negotiate With a Bank to Reduce the Interest Rate

Try negotiating directly with your creditor to reduce the interest rate and monthly payment. All it takes is a simple and quick phone call in many cases. You may even convince a creditor to lower your interest rate permanently.

Here’s a simple script that you can use to negotiate with your creditor.

Call your creditor and ask to speak with a Supervisor because only a Supervisor will have the authority to make these changes. Say the following:

“Hello ____, how are you today? I’ve been a loyal client for ___ years and have always paid my bills on time, so I hope you can help me today so that I can keep my credit card account open with your bank. Your hands may be tied, and you may not have any power to help me here, but I figured I’d try to communicate openly with you about this matter before closing my card. I want to stay with your bank as you guys have always been good to me. Anyway, here’s my situation; _______ bank offered me a ___% interest rate on a similar card with 3% cashback included. Since this interest rate is ___% less than what your card is offering me, I’ve decided to close this card out and switch to the new card that ____ bank is offering me. Unless you can reduce my interest rate or upgrade my card to match what _____ bank is offering and offer me some similar cashback. What do you have the power to provide me with today to help me out? “Then go silent.

6. Credit Card Hardship Program with Bank (e.g., Chase, Bank of America & Citi)

In some cases, you may only be able to get a temporary reduction in the monthly payment, but if you’re going through financial hardship (like many consumers are due to COVID-19), that may be your best solution.

To be considered for a bank’s credit card hardship program, you must be behind on your monthly payment, but not to the point where your credit report is negatively affected. Some banks may have also extended COVID-19 debt-relief options but only consider one of these plans if the creditor is willing to pause the interest and payment. Otherwise, the interest continues accruing and gets tacked on to your existing balance, making your debt grow even larger. Credit card forbearance and deferment options are only worth considering if the interest is reduced or paused.

Steps to get approved for your bank’s credit card hardship program without a negative effect on credit scores

- The trick is to call your creditor 7-10 days after you miss the monthly payment. Unfortunately, late payment history isn’t reported to the credit reporting agencies until you’re more than 29 days past due.

- To strengthen your case, send the creditor a copy of your budget analysis, a financial hardship letter, and evidence to validate your reason for needing a lower payment before calling them.

- When calling your creditor, request to speak to a supervisor because they can reduce your monthly payment. Let the supervisor know that you’re calling to see if they can temporarily lower your monthly payment. Go over the fact that you could not afford to make your last monthly payment and explain why. Include the details of your financial hardship. Make sure to keep your story following what you stated in the hardship letter. Also, reassure your creditor that your financial problem is only temporary and provide an estimate for how long you’ll need the relief.

- The supervisor will ask you a series of questions about your income. At that point, verify that they received your budget analysis, hardship letter, and whatever documentation you sent. Then, use this free budget calculator to create your budget.

You’ll be rejected from a bank’s credit card hardship program if your income is too low due to insufficient income. On the other hand, if your income is too high, they may not consider you a genuine financial hardship. There is no set number, but as a general rule of thumb, consider showing that you could reasonably afford about half of the projected monthly payment that is currently required.

7. Debt Validation Plans Last For Three Years (average)

How can I get out of debt without paying? This next option is your closest route to getting out of credit card debt without paying. After invalidating credit card collection accounts, that collection agency can no longer legally come after you.

Debt validation can’t magically erase your debt. H

Noach Dear, a New York Supreme Court Judge, estimated that 90% of credit card lawsuits are flawed and can’t prove the person owes the debt.

Possible Reasons Why a Debt Could Become Invalidated

- Unauthorized fees get added in, making it impossible for a collection agency to prove the debt is valid.

- The collection agency may not produce a valid debt collector’s license for a particular state.

- Paperwork gets lost or missing documentation, like a collection agency may not produce the original agreement signed when the consumer first applied for the credit card.

- Incomplete records get transferred from the original creditor to the collection agency.

- The statute of limitations on a debt may have expired, or collection agencies can’t supply accurate information about when the statute of limitations is set to expire. Remember, for an account to be “valid,” it must be legally verifiable with complete and accurate records after being requested.

- A collection agency may not be able to produce accurate information.

8. Debt Settlement Services to Get Out Of Credit Card Debt in Under Four Years

If you can’t afford to stay current on your credit card payments, debt settlement can reduce the balances and allow you to clear your credit card debt in around three to four years.

Let’s look at an example:

A debt settlement program could resolve $50,000 worth of credit card debt for $30,602. When paid over three years, that would result in a monthly payment of $850.

Versus:

When paying minimum payments on $50,000 of credit card debt, the monthly payment would be around $1,400, and it could take approximately six years or longer to pay the debt off in total (depending on the interest rate).

As you can see, debt forgiveness programs can offer a much lower monthly payment for consumers struggling to pay their credit cards.

Additionally, you can avoid bankruptcy.

Try this debt calculator to see your options:

Negative consequences of debt settlement include:

- Credit scores go down, and derogatory notations appear due to creditors not getting paid every month (including late and collection marks).

- There is no guarantee that a creditor will settle at a certain percentage.

- The IRS could require paying taxes on the amount saved after a credit card settlement.

- Late fees and interest can cause balances to increase over the program’s first year.

- A creditor could issue a person a summons to go to court; although this is rare, it could happen.

9. Consumer Credit Counseling to Pay Off Credit Cards in Less Than Five Years

If you can’t pay off credit card balances due to high-interest rates, consumer credit counseling could be your best solution.

A consumer credit counseling (CCC) plan, also known as credit card consolidation, may lead to lower interest rates and consolidate several of your monthly payments into an easier-to-deal-with, more manageable single monthly payment.

It’s common to see 25% interest rates reduced to 8%-10%. In addition, consumer credit counseling can lead a person out of credit card debt within 4-5 years versus 9-15 years when paying minimum payments.

Although participation in CCC has a minimal effect on a person’s credit score, future creditors may see that you used this type of debt assistance.

For example, your credit rating has an adverse effect when you change the original terms of your credit card contract. And with consumer credit counseling, a third-party notation gets reported on your credit report. Lastly, credit cards are closed out after joining a consumer credit counseling program, negatively affecting credit scores.

The good news is that with consumer credit counseling, you don’t have to fall behind on payments, like with debt validation and settlement programs.

10. Chapter 7 Bankruptcy Can Clear Credit Card Debt in Under 6 Months

Why is Chapter 7 the preferred way of bankruptcy?

The reason is that Chapter 7 bankruptcy wipes away credit card debt, so it doesn’t have to get paid.

Chapter 7 bankruptcy only lasts for 3-6 months, making this one of the fastest ways to clear credit card debt in 2021.

With chapter 7 bankruptcy (also known as “liquidation bankruptcy”), a debtor’s assets are sold, and the proceeds are used to pay off creditors. However, 95% of debtors do a “no asset filing” because they don’t have any assets to be sold. If a debtor doesn’t have any assets to get sold, their debts are discharged and no longer legally owed.

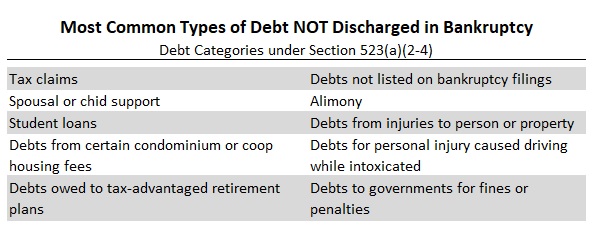

Credit cards, private student loans, medical bills, and almost all unsecured debts can get discharged and wiped away clean (excluding federal student loans, tax claims, spousal or child support, condominium and housing fees, alimony, and a few others).

Debts NOT Discharged in Chapter 7 Bankruptcy

The Downsides of Bankruptcy:

- Your credit score can get lowered by 175 points.

- Next to each creditor that gets discharged will say, “debt discharged due to bankruptcy.”

- Potential employers, landlords, and creditors will all be able to see that you filed for bankruptcy.

- Credit scores will be subprime after filing for bankruptcy, making it difficult to get approved for low-interest rates on any credit.

- Premiums on car insurance, cell phone, and monthly insurance payments can all legally increase once bankruptcy goes on a person’s credit report.

- Chapter 7 bankruptcy can stay on your credit report for ten years

Here’s a bankruptcy guide to help you learn more about bankruptcy if this is an option you’re seriously considering. But remember, a settlement program is a smart choice for consumers to explore before deciding on BK to clear their credit card balances.

Great post on how to get out of debt. Thank you

Hello everyone, im from Missouri USA, I have been struggling looking for a means of getting a loan for the past 4 months, I have searched a lot of companies. I needed a loan of $47,000 to set up a business and settle my bills as well as take care of my children. I can’t get approved for a loan anywhere, what should I do?

Hello Nancy, you mentioned that you need a loan to settle your bills, are these collection accounts? If so, I would recommend you use debt validation to dispute the collection accounts in an effort to get them off your credit report. Don’t just dispute the debts through the credit reporting agency because they can easily get validated and will then show an unsuccessful dispute had occurred, further damaging your credit score. Validation could resolve the debts and potentially lead to them coming off your credit report if the collection agencies can’t prove the debts are valid. If the debts are proven to be valid they could always get settled for about half of the amount owed if the collection agency agrees to remove the debt from your credit entirely upon payment received on the settlement. You can get a free credit report at annualcreditreport.com and then have one of our specialists take a look at it for you and see what your best options would be. The debt validation program won’t charge you anything if the account is proven valid so it can’t hurt to give it a try!

Nancy, check out Missouri Debt Relief Programs https://goldenfs.org/missouri-debt-relief/. That page may be more relevant to your situation since you live in Missouri. Give us a call if you do need help.