The following blog post is a summary of the book, Common Stocks and Uncommon Profits by Philip A Fisher, one of the best investing books of all time. Fisher was an early advocate of growth stock investing, like how Benjamin Graham is to value investing.

The following blog post examines:

- The 15 criteria used to find the best growth stocks

- Powerful forces that can affect market prices

- The Best Quotes from Philip Fisher About Investing in Stocks

- When to sell a stock to make the maximum profit

- The Truth About Dividends

How to find the best stocks to buy:

In the book, Common Stocks and Uncommon Profits, a checklist of fifteen points is provided on how to buy the best growth stocks. In general, the advice on buying growth stocks, as explained in the book, is based on a combination of quantitative and qualitative factors.

15 Points to Select Growth Stocks That Can Make the Greatest Possible Gain.

- Products and Services: “Does the company have products and services with sufficient market potential to make possible a sizeable increase in sales for at least several years?” Look for companies with a great management team, that are constantly innovating and creating new products.

- Attitude: Does the company’s management have a determination to continue to develop new products that will further increase total sales when the growth of currently attractive product lines begins to decline? Companies that have a significant growth prospect for the next few years but nothing beyond that, including a lack of processes in place by its management team to continue to expand, may offer only one-time or short-term profits. Companies must be able to grow their products over time, like how a tree grows and how the branches continue to branch off and grow higher and higher. Stay away from businesses that acquire unrelated products in a desperate attempt to grow, buying businesses that end up failing as branches die on a tree. Instead, look for companies that continue to expand their operations by acquiring competitors or related businesses and continue creating and innovating. A company should have research and engineering departments continually working to improve old products and develop new products.

- Research and Development: Does the company spend a decent amount on research and development, which translates into a sizeable increase in net profits and sales in relation to its size? Compare the ratio of a company’s research and development spend to their net profit over an extended period (i.e., five to ten years or longer). Divide the research figure by total sales to determine the percent of each sales dollar spent on research. Compare this ratio to other companies in the same industry. Are they spending more than other companies on research? Is that research resulting in more profits compared to other companies in the same industry? Or, is the amount of revenue being spent on research abnormally high, and it’s not resulting in increased revenue and income at a rate similar or better than other companies in the same industry? Examine the details and ask the right questions. Fisher says the best-run companies will get twice the gain for each research dollar spent.

- Sales: Does the company have an above-average sales organization? Repeat sales to satisfied customers is the first confirmation of success for any business. Outstanding production, sales, and research are the three most important aspects of a successful business.

- Profit Margins: Does the company have the best profit margin in the industry? Don’t check for just a sudden short-term boost in profit margins that end up being temporary. Look at a company’s profit margins over a five to ten-year period. Also, search for a company with steadily improving profit margins and return on equity. Microsoft is an example of a company with improving profit margins over the last decade. A deviation from this rule is if a company decides to invest all or most of what would generally be profit into research or growing their sales. That extra research and the expenses put towards growing sales will boost productivity and revenue in the future. Keep in mind that the weaker companies may boost profit margins during good years but will normally have low-profit margins, so don’t get fooled.

- Cost Cutting and Product Engineering Departments: Is the company working to improve profit margins? If so, how? Are they cutting costs? Look for companies with capital improvement and product engineering departments that focus on designing new cost-efficient equipment and innovating or utilizing economies of scale. For example, accounting firms can develop new software to replace manual accountants and drastically reduce costs. Shipping companies created new containers to ship products more cost-efficiently and create branch offices to avoid cross-hauling. Fisher states that rising wages result in increases in the cost of raw materials and supplies, putting pressure on a company’s profit margins. So, what can a company do? Companies can raise prices to offset rising wages and expenses. Or, an even better long-term solution to improve profit margins would be to maintain product engineering departments to design new cost-efficient equipment. Consider these points to create the right questions to ask about a company.

- Labor Relations: Does the company have outstanding labor relations? Look for companies with the best employee retention rate; they have strong personnel relations and labor relations, treat employees with respect and dignity, and make employees feel important. Compare labor turnover in one company over another. Look for companies with good labor and personnel relations. The best companies will have a waiting list of people wanting to work for them. Companies with good labor relations look to settle disagreements quickly. Companies that make above-average profits and pay above-average wages usually end up being excellent investments. Currently, sites like Glassdoor illustrate employee reviews. Companies like Salesforce, Google and Amazon, are all highly rated employers. Stay away from companies that have high-profit margins in part because they pay below-average wages. Fisher stresses, try to collect feedback about a company from its ex-employees.

- A Company’s CEO and President: Does the company have a highly-respected CEO and president? Look for companies with respected CEOs and presidents. Elon Musk comes to mind. Tesla’s executives have confidence in their president.

- A Management Team with Depth: Does the company have a deep and layered management team? Look for companies with depth in management; there’s not one owner of the company running it all. There are specialized departments with experts heading each. Also, top management should welcome feedback and ideas from personnel.

- Cost Analysis and Accounting Policies: How good are the company’s cost analysis and accounting policies? Look for companies that can break down the overall costs with accuracy to show the cost of each small step in its operations. Only in this way will a management team know what products are most profitable and which need improvement to maximize overall profitability. Companies can then also understand which products deserve special attention for additional sales promotions. The best management teams understand the importance of having top expert accounting control and cost analysis.

- MOAT: How much of a MOAT (i.e., competitive advantage) does a company have over its competitors? Consider patent protection at times, but don’t place too much emphasis on it. The constant leadership in engineering, not the patents, is the fundamental source of protection. What competitive advantages does the company have?

- Relationship with Suppliers: Does the company have established relationships with suppliers allowing them to get better deals than their competitors? These relationships can result in long-range profits. Compare a company’s expenses against other companies in the same industry with certain suppliers. If a company can get certain supplies at a lower cost than its competitors, perhaps through economies of scale, it will most likely have a surplus of profits over the long term.

- Cash and Top-Notch Credit: Beware of companies that don’t have sufficient cash, strong credit, and borrowing abilities. These companies may need to raise cash through equity financing, which dilutes the per-share earnings and could cause a drop in the stock price. The best investments are in companies that have sufficient cash and borrowing abilities to fund their future growth. Look for companies with the best credit ratings in their industry, lots of cash (preferably enough cash to pay off all long-term debt in under a few years), and that have illustrated a continual increase in free cash flow over a five to ten year period. Also, examine a company’s current ratio. The current ratio is a measure of short-term liquidity. The best stocks have a current ratio above 1.5%. Too high of a current ratio can mean that a company is struggling with finding the best opportunities to reinvest in.

- Transparent: Is the company transparent about bad news, or does it clam up and try to hide bad news? Stay away from companies that don’t report as freely when things are going poorly as when things are going well.

- Integrity: Does the company have a management team that operates with integrity? One way to tell if a management team lacks integrity is to do a Google search of insider names that have purchased shares from the company, with fraud or scam in the search query. It’s undoubtedly a red flag if you find an insider of a company was involved in anything related to securities fraud in the past. You’ll be surprised to see how often insider names are associated with fraud, particularly amongst smaller companies with less established earnings. A few ways to determine if a management team lacks integrity is to see if they have family members on their payroll that get above-average salaries for the work being performed or own properties rented to the corporation at above-market rates. Insiders may also issue stock options to themselves that are outrageously high and clearly biased.

Click Here to Get Your FREE Common Stocks and Uncommon Profits PDF Book Summary

Related Posts:

- How to Earn $50K Per Year Off Dividend Income (16 Best Dividend Stocks)

- One Up On Wall Street by Peter Lynch (Book Summary)

- How to achieve financial freedom

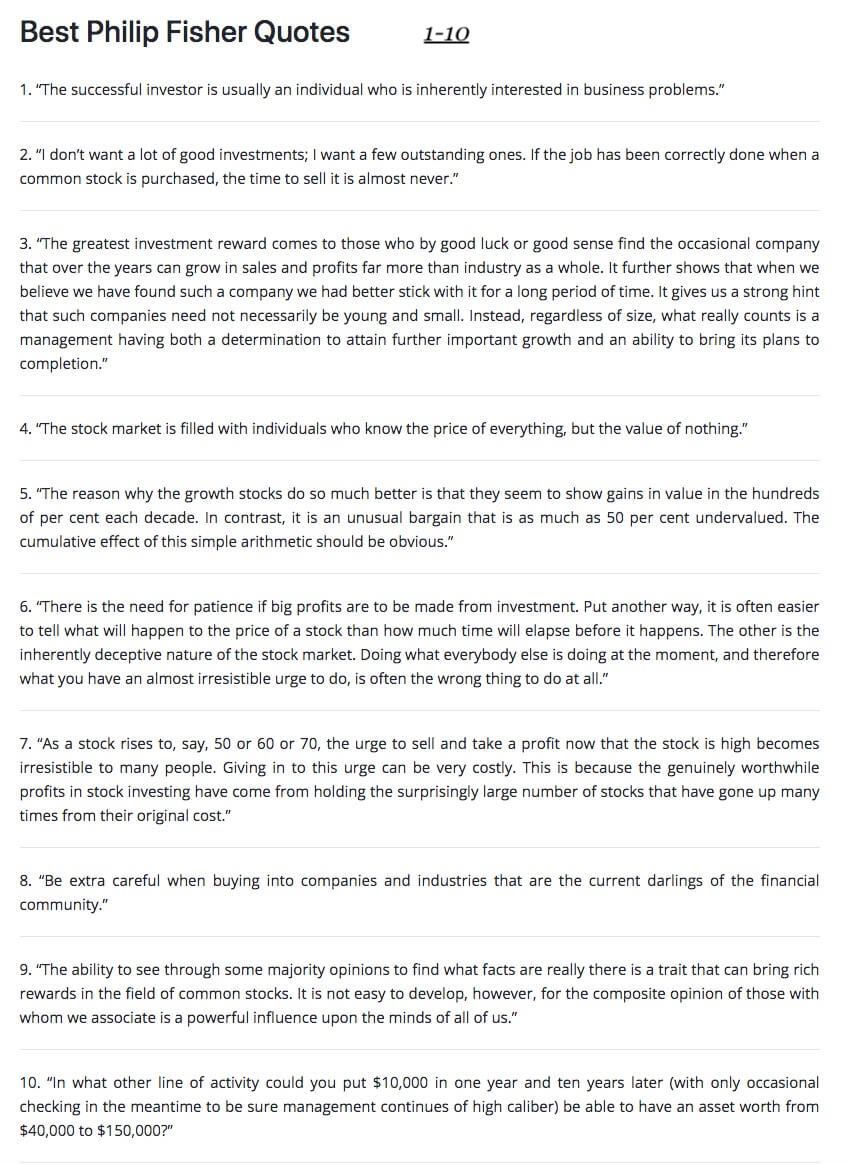

Top 10 Quotes by Philip Fisher About Investing in Stocks

Invest in a company over several years, not all at once.

When you’re ready to invest in a company, invest incrementally over several years.

By doing so, you’ll minimize your risk and be able to take advantage of investing in low prices if a market downturn does occur.

You can avoid risking investing all your money right before a market downturn, which nobody can predict, not even Warren Buffet.

For example, if you invested in Apple, Google, or in many other companies right after COVID-19 hit in March 2020, you would have doubled or tripled your money by mid-2021.

When to buy growth stocks?

Towards the end of the book, Common Stocks and Uncommon Profits, Fisher summarizes when to buy growth stocks.

He says: “Focus on buying growth stocks when they are out of favor; that is, when, either because of general market conditions or because the financial community at the moment has misconceptions of its true worth, the stock is selling at prices well under what it will be when its true merit is better understood.”

5 Powerful forces that can affect stock prices:

In the book, Common Stocks and Uncommon Profits, here are the five powerful forces that were revealed that can affect stock prices:

- The current phase of the business cycle (e.g., Stocks in cyclical industries, like the car industry, sell for high price-earnings ratios for a period, and then low price-earnings ratios. These different periods can last for several years.)

- Government attitude towards industries and investments. (e.g., If you bought Tesla in 2020, government attitude toward clean energy would have helped your investment in Tesla skyrocket.)

- Inflation (e.g., The cost of gas rose, and so did Exxon Mobile stock.)

- The direction of interest rates (e.g., Low-interest rates can help stock prices continue to rise because lower interest rates (A) make it easier for companies to pay off debt, increase net income and improve profit margins (B) provide an incentive to borrow at low-interest rates and invest in growth and (C) makes bonds less attractive resulting in more investors leaning towards stocks.)

- New inventions and techniques that can affect older industries (e.g., Netflix came out, and Blockbuster closed. Bitcoin was invented and gold became less attractive.)

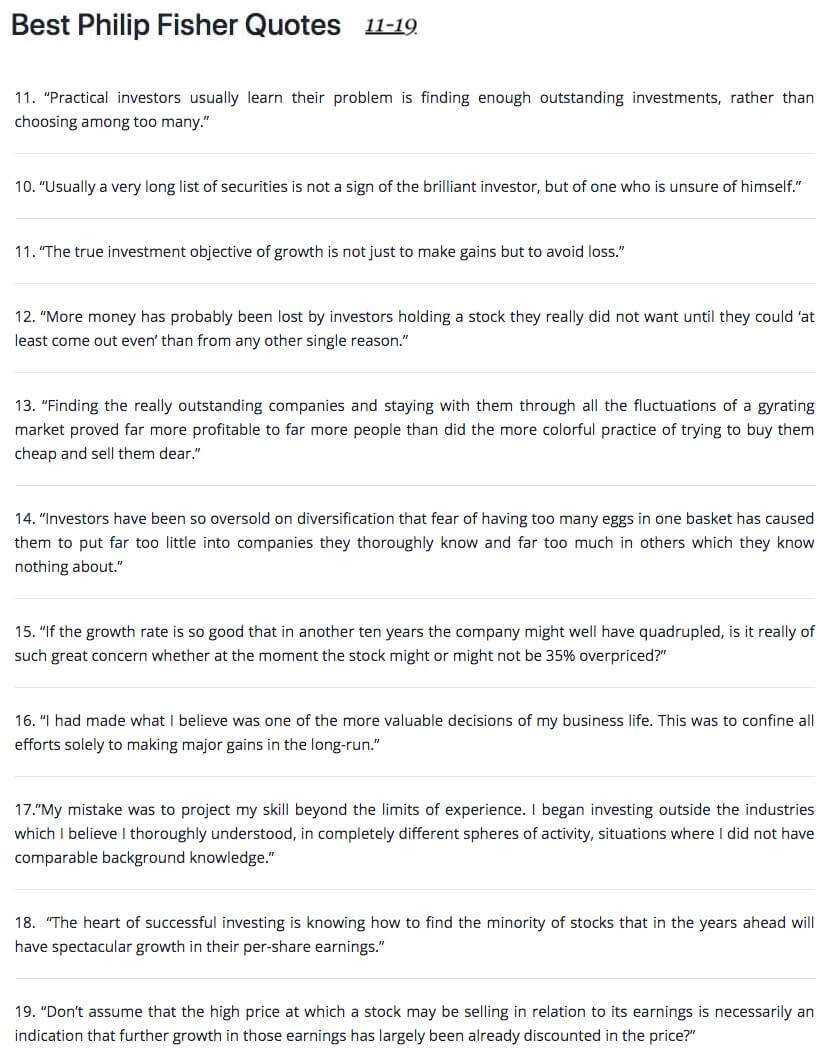

More Quotes from Philip Fisher

Finally, meet up with the company’s management team.

Fisher stated in the book that, by the time he meets with a company’s management team, there’s a 50% chance that he will invest in that company because they already checked off on the fifteen qualifying points mentioned above.

A critical question Fisher will ask any top executive at a company he is considering buying, is the following: “What is the most important long-range problem facing your company?”

Make sure you are prepared with the right questions when it’s time to meet up with the company’s management team, don’t mess this up!

Is it worth the time to research companies to check that they pass each point on this list?

You can put $10,000 into a great company today, and in ten years, that $10,000 would have grown to anywhere from $40,000 to $150,000 without you even having to look at it over the ten years. Yes, it’s worth the time! Where else can you earn money like this?

When to sell a stock to make the maximum amount of profit:

When to sell, Point 1:

When you made a mistake in picking an investment, sell the stock (sooner than later.)

Emotional triggers can make you hold onto a losing stock, in the end, costing you more than if you had sold early.

You must be able, to be honest with yourself and not go into denial. You can write off some of the losses, so in the end, they may not cost you a dollar.

Example of how to cut your losses:

Let’s say you buy three stocks adding up to $100,000, each for around $33,000. You made 25% over three years, so your investment turned into $125,000 from just these three winning stocks.

You also bought a fourth stock for around $33,000, the same price as the others, but this one stock lost 25% of its value before you finally sold. So, in the case of the losers, you lost $8,250. And from this, you can write off $5,000 of it, so you only lost $3,250.

The point is, it’s OK to have losers if most of your investments are winners, but it’s critical to learn how to cut your losses and sell before you lose more than you need to lose.

In this example above, if you held on to the loser until the stock lost 75% of its value, you would have lost $24,750, almost eating away all your investment returns.

But what if you cut your loss at around 12%, you would have only lost $3,960. You could then write off the entire loss of $3,960, so in the end, you didn’t lose a cent! And in fact, you can turn that loss into a learning experience, helping you avoid making the same mistake in the future and becoming a savvier investor.

When to Sell, Point 2:

It’s time to sell when the stock no longer qualifies for the fifteen points mentioned above. Sometimes a new management team comes in, and the entire company deteriorates. Or, with growth stocks, perhaps the company exhausts its growth prospects.

When to Sell, Point 3:

In the book, Common Stocks and Uncommon Profits, the author summarizes this third point as such:

“If opportunities for attractive investments are extremely difficult to find and the companies you own appear less attractive as well, it may be worth selling and paying your capital gains in order to switch into an investment with better prospects.

For example, a company that pays 12% for several years can provide very attractive annual compounded returns. However, if you can find a company that could produce a 20% return annually, it would be well worth selling your existing stock that’s paying 12% annually, paying the capital gains, and switching to the new company that could produce a 20% annualized rate of return.

Don’t sell a stock just because it went up a significant or even a tremendous amount and temporarily has a high price-earnings ratio. Great companies keep getting better, and price-earnings ratios come down as earnings continue to grow.

In February 2018, Google’s price-earnings ratio was above 60. Since then the stock price has only gone up and in 2021 its price-earnings ratio was under 30.

Just look at Google, Amazon, Apple, and Microsoft. At one point, these companies all had high price-earnings ratios.

Consider the following analogy, as explained in the book, Common Stocks and Uncommon Profits.

Suppose it was your last day of college or high school. Now suppose on this day, each of your classmates had an urgent need for immediate cash. Each offered you the same deal. If you gave them a sum of money equivalent to ten times whatever they might earn during their first twelve months after they had gone to work, that classmate for the rest of their life would pay you twenty-five percent of each year’s earnings.

While you loved the idea of this deal, you only have enough cash to make such a deal with three of your classmates. At this point, your reasoning would closely resemble that of the investor using sound investment principles when selecting stocks to buy.

You immediately start analyzing your classmates solely based on how much money they might one day earn.

You would eliminate a lot of your classmates just based on not knowing them well enough to be able to pass such judgment as to whether or not they will (A) one day make a lot of money and (B) be trustworthy enough to pay you as agreed.

Here again, the analogy with intelligent common stock purchasing runs very close. Eventually, you’ll pick the three classmates that you felt would have the greatest future earning power.

Should I sell just because the price-to-earnings ratio is high?

Ten years have passed. One of your classmates has done sensationally. He went to work for a large corporation and has won promotion after promotion. Insiders at the company say that the president has his eye on him, and in another ten years, he’ll probably be CEO at the company. He will be in line for a large compensation, stock options, and pension benefits that come with the job.

So, at this point, you’ve already made a 600% return. Would you sell your contract with your current classmate just because you got a good offer and could cash out making 600%? Or, would you keep this contract for another ten years, knowing your classmate will continue to grow their income over time? Anyone telling you to sell, so that you could switch your contract to another classmate making about the same as what they were making on that last day of college, would need to have their head examined.

When researching stocks, think in a similar way. Don’t just sell a stock because you made a bunch of money already.

Common Stocks and Uncommon Profits: Summary of When to Sell

If you properly selected the right stocks to buy, “the time to sell is – almost never.”

The Truth About Dividends

Companies that are growing in value don’t usually pay a dividend or pay a small one. Instead, fast-growing companies reward shareholders by increasing in value. Instead of paying a dividend, growth companies will retain earnings and use the earnings for growth-related activities, such as installing cost-saving equipment in an old plant to improve profit margins, opening more offices or stores, and launching new products.

But what happens when growth stocks stop growing so fast? What if a company goes from increasing its earnings at an annualized rate of 25%, to less than 7%? At this point, will it benefit the company’s shareholders for the company to continue retaining its earnings or pay more out in dividends so its shareholders can collect income?

These could be good questions to start asking.

Let’s take a closer look.

When is it OK for a company Not to pay dividends?

Is the company retaining its earnings, rather than increasing its dividend, only to pile up cash or increase their own managements’ salaries? First off, “managements with such inefficient and substandard operations would have failed to qualify under the fifteen points mentioned above.”

Is the company using the retained earnings to replace or buy assets that would not translate to increased earnings? Like for example, maybe stores are buying air conditioners for every retail store across the nation? This is only going to restrict growth temporarily and is a necessary expense, so it’s acceptable.

Without adding air conditioners in every store, these stores may get less business in the summer months. So, understanding what a management team is using the retained earnings for will help you better judge if they’re using the money wisely, and if the investments being made will result in increased profit down the road.

Earnings can fluctuate, even some years going down. That’s normal.

In other cases, like with Intel in 2021, they’re using retained earnings to invest in building new plants. These earnings are being well spent, especially since there’s a shortage of specialized chips. With new plants, Intel can make more chips and take over additional market share, increase revenue and grow return on equity.

Eventually, this investment by Intel will reward its shareholders, resulting in increased revenue and earnings. And remember, a stock’s price will follow the path of its earnings.

If earnings of a company continue to rise like a hill over ten years, most likely, the stock price will do the same.

However, using money to add new plants won’t increase earnings for several years out. So, examine if the lack of increased profits is temporary and see where the company is spending money before jumping to conclusions.

Try to see the full picture several years out, knowing new plants are being built to expand products due to heavy demand, which will bring additional earning capacity for the long-term. By visualizing this information put into perspective, you’ll realize that the stock is only down temporarily, and by investing in it today you can experience the most profitable route.

You can gather the insight to be able to project earnings into the future by properly evaluating management’s plans and processes, its research and development expenses, and future growth prospects.

Can it be a bad thing when a company raises its dividend?

Fisher stresses, sometimes a high dividend payout can be a red flag, indicating a poor management team. For example, suppose a company can’t find attractive ways to use their retained earnings, so instead, they raise the dividend. Well another way to examine this point, is to check a company’s current ratio.

A current ratio of 1.5% to 7%, shows a company has liquidity. But any higher than 6-7% could illustrate the company is having difficulties finding places to invest their extra money. Why is the cash just piling up, rather than being invested towards growth and acquisitions, or at least a portion of it being paid towards increasing the company’s dividend?

Slow growth companies suddenly can’t think of new products to create or ways to innovate. Moreover, their existing products no longer have heavy demand and appeal. Consequently, they have no further need to open new stores and plants.

Fisher says, “What is most important is that stocks are not bought in companies where the dividend payout is so emphasized that it restricts realizable growth.” Fisher feels that companies should pay a dividend, but not too high of a dividend.

Dividend Payout Ratio

Examine the payout ratio for the dividend.

The payout ratio is the percentage of net income being paid as a dividend.

If 70% or more of the net income is getting paid out as a dividend, this can be a dangerous situation.

Suppose interest rates rise and net income falls by 30% or more, that company could be in jeopardy of being able to afford to pay their dividend. They may then have to cut their dividend, resulting in the stock price falling and you losing money in multiple ways.

10 Dont’s for Investing:

- Don’t buy into promotional companies (i.e., Only invest in companies with at least one year of earnings and several years of successful operations, no matter how attractive the picture is that they’re painting.)

- Don’t not buy a stock because it’s over the counter. Use the same 15 rules above to select the best stocks to buy, even if they are over the counter.

- Don’t buy a stock because you like the tone of its annual report. These reports can be written by a public relations department that does its best to make the company look good. Even though the president of the company signed off on the bottom of the annual report, doesn’t mean he wrote it.

- Don’t assume that if a company has a high price-earnings ratio, further growth in those earnings has largely been already discounted in the price.

- Don’t fuss over a few dollars or cents when contemplating investing in a great company. If you find a great company selling at a fair price, start investing in it right away. Don’t wait for it to go down another fifty cents because it may never go down, and then what happens if it goes up tenfold? You could look back one day saying that you missed the best opportunity in your life which could have made you millions of dollars, over fifty cents per share.

- Don’t overstress diversification. Fisher feels that by investing in too many stocks, you can’t keep track of all your investments and you may end up with lots of investments that amount to very little profit. It’s more dangerous to invest in companies you don’t know and understand very well just to be able to say that “you’re diversified” than having inadequate diversification. Fisher suggests that one could diversify by investing in five different stocks that don’t overlap in any industry and putting 20% of your funds in each. Fisher strongly advises against holding more than twenty different stocks. He feels if you have over twenty different stocks, it’s a sign of “financial incompetence.” If you own more than twenty stocks, work to “complete a move toward concentration.” Over several years, work towards selling your least attractive investments and moving the funds into your most attractive stocks.

- Don’t be afraid of buying stocks on a war scare.

- Don’t worry about the stock’s past high and low. None of it matters. What is the company going to do in the future?

- Don’t follow the crowd.

- Don’t fail to consider time as well as price when buying a growth stock.