You can achieve wealth and financial freedom in your future, no matter what your situation looks like today. You just need some sound financial advice and that’s what I’m about to give you!

Inside this post, we provide new and innovative ways to increase your income, have excellent credit and stellar financial health.

Everything you do in life starts with steps. When you’re a baby, you need to take your first few steps to walk and then soon after you’re walking on your own, and eventually running wild.

With your finances, you have to take that first step as well, and then the next, and eventually you keep growing financially.

Start by reading this post and immediately after implement at least one point on this list.

Also, new laws passed that will allow American’s a chance to save more for retirement. The details of these law changes will also get revealed.

The author of this post, Paul J Paquin, is an entrepreneur and the CEO at Golden Financial Services.

Mr. Paquin provides his best financial tips inside this post, to prepare consumers for a prosperous new year.

Tip 1: New Law Change: IRA Contributions Increase

As of 2019, you can invest up to $6,000 per year into an IRA.

Before 2019, you could only invest up to $5,500 per year into an IRA.

Tip 2: Invest Weekly, Not Once Per Year

Dollar–cost averaging (DCA) is an investment strategy, where you buy a fixed dollar amount of a particular investment on a regular schedule (like weekly, or bi-weekly), regardless of the share price. By using dollar-cost averaging, you’ll end up buying more shares when prices are low and fewer shares when prices are high, minimizing your chances of losing money.

- Invest $125 per week, which will get you to the $6,000 limit for 2019

- Set up autopay so that automatically $125 per week goes into your Roth or Traditional IRA

Tip 3: What’s better, a Roth or Traditional IRA?

I prefer the Roth IRA because I would rather pay the taxes now, when the funds are at their smallest, and not have to worry about paying taxes later in life. However, you will also need a Traditional IRA set up through your employer, to benefit from a SEP or 401(k).

Why open a Roth IRA?

- You pay the taxes when the funds are at their smallest, right when you initially invest the money, allowing you to pay the least amount of taxes.

- Watch your money grow, TAX-FREE, and withdraw it without having to pay taxes when you’re retired.

- FLEXIBILITY: “Roth contributions can be withdrawn penalty-free at any time”, according to Maria Bruno, CFP professional and senior investment analyst with Vanguard’s Investment Strategy Group. You can make withdrawals from your Roth IRA prior to retirement and without a penalty, if you are using the funds to pay for certain “emergency-related expenses”, like disability-related, or for a first time home purchase of up to $10,000, and postsecondary education, and there are a few other exceptions that you can read about here.

Why open a Traditional IRA?

- Since you’re investing before the taxes come out, more of your money gets put to work. When you’re ready to use the funds during retirement, you will have to pay the taxes at that point.

- A business offers either a 401(k) or SEP-IRA to their employees. Both of these types of retirement accounts are connected to a Traditional IRA, allowing your employer to invest your money before the taxes come out.

- Most people are in a higher income-bracket when they are younger, so would rather pay the taxes later in life when they anticipate being in a lower tax bracket. In this case, the traditional IRA would benefit you more than the Roth.

Tip 4: The Power of Compound Interest

What is “compound interest”? Compound interest is when you earn interest on your total accumulated funds. (i.e., Regarding investing in a Roth IRA, your first year you are only receiving 10% on $6,000, which is $600, but the following year you’ll earn 10% off $12,600, giving you $1,260 in tax-free earnings. The third year you’ll make $1,860 off your investment, and so forth!

According to Wikipedia: “Compound interest is the addition of interest to the principal sum of a loan or deposit, or in other words, interest on interest. It is the result of reinvesting interest, rather than paying it out, so that interest in the next period is then earned on the principal sum plus previously accumulated interest. Compound interest is standard in finance and economics.”

Thanks to compounding interest, if you are 28-years-old and invest $6,000 per year into a mutual fund that earns 10% per year on average, you will be a millionaire by the time you reach 60 years of age.

Tip 5: Credit Card Debt (3 Points You Need to Know)

Never carry a balance on your credit cards.

First of all, if your balance is over 35% of what your credit limit is, your credit score will be negatively affected. As your balance grows on a credit card, your credit score goes down.

Second: when you carry a balance on a credit card, you pay interest every month.

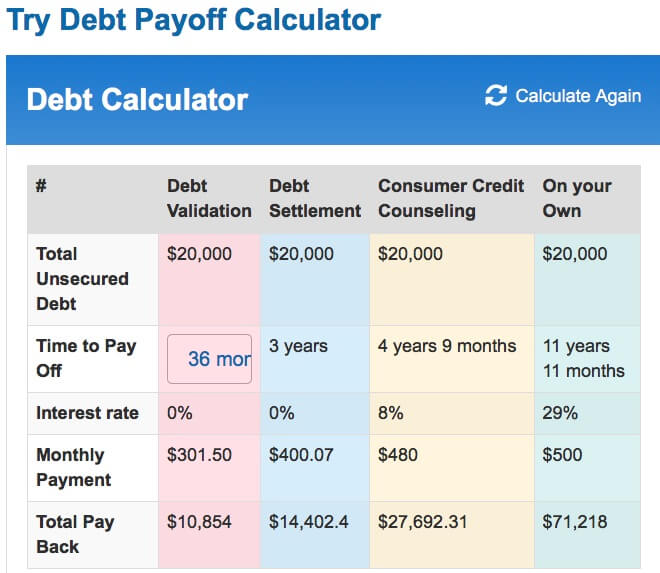

If you have $20,000 in credit card debt, with a 29% interest rate, when paying $500 per month towards this debt it would take you 11 years and 11 months to pay the debt in full. And, you’d end up paying $71,218 in total (including interest). Here is the debt calculator that we used for this calculation if you want to try it yourself.

Wow, that’s well over double what your debt was worth in the first place!

You would be just as well-off, by flushing your money down the toilet, as you are when carrying a balance on your credit cards and paying interest every month – it’s a complete waste of money.

By paying your credit card balance in full every month, you avoid 100% of interest.

Third: for the savvy financial wizards out there, by paying your balance in full every single month, you can increase your income by earning cash-back from your purchases that month.

Make sure you have a card that pays you at least 2% cash-back on all purchases, especially including gas and groceries, and at all of your favorite stores that you shop at most often – it’s free money, why not take it!

You may need to have 4-6 credit cards in total, to earn cash-back on all of your purchases. But that’s free money, so get it!

Tip 6: Increase Your Credit Limits & Score

Increase your credit limit at least once per year on each of your credit cards.

As your available credit increases, your credit score goes up.

As you pay down your credit card balances, the reason that your credit score goes up is that your credit utilization ratio improves simultaneously.

Your credit utilization ratio is “how much credit you have.”

Tip 7: Hire a Competent Accountant

Hire a competent accountant who knows how to write off expenses to reduce a person’s tax liability. Having one child can offer lots of tax reductions. If you have two children, you have twice as many write-offs.

So many people pay more in taxes than what they need to pay if they only hired an accountant who had a better understanding of the tax laws.

Do you have any mutual funds that took a loss this year? If so, you can use what’s called “tax harvesting.” Tax harvesting is selling off your losing stocks and mutual funds that took a loss this year, and you can then use these losses to offset gains from the sale of winning investments.

Tip 8: New Law Change: 401(k) Contributions Increase

Ask your employer about how you can invest in a company 401(K). Most employers will match your investment.

As of 2019, you will be able to invest up to $19,000 per year into a 401(K).

Tip 9: New Law Change: For Seniors With an IRA

If you are older than fifty years of age, you can now invest an additional $6,000 per year into your IRA. The IRS lets you play catch-up for past years that you forgot to contribute.

Tip 10: Own a Business?

A lot of small business owners never open a 401(k) because it’s complicated and expensive. A SEP-IRA is an alternative to a 401(k) for a small business owner, and it’s easy to open, plus free!

The limits are even higher than a 401(k), and a SEP is much easier and quicker to set up.

With a SEP-IRA you can invest up to $54,000, or 25% of your qualifying income, per year.

Tip 11: Max-Out a 529 Plan For Retirement

With a 529 plan, each parent and grandparent can contribute up to $14,000 per year. The funds invested in a 529 plan are tax-free if used for educational purposes.

You can also make additional gifts for medical, dental, and tuition expenses that do not count toward the $14,000 limit as long as you make those payments directly to the provider.

In addition to federal tax savings, 34 states offer state income tax deductions for 529 contributions. If you’ve had a bunch of money blown your way this year, you can also take advantage of up to five years of gift tax exclusions to set aside up to $70,000 in a 529 plan in a single year.

It costs over $60,000 per year to send your child to college (on average).

It’s never too early to start saving for college.

Tip 12: Buying Delinquent Property Tax Liens (to Make $$$)

Imagine being able to buy a $300K house, for $10,000.

You can.

Even if you can’t afford to buy a house, have you considered buying delinquent property tax liens? You will have to first read about your state’s laws before investing in delinquent property tax lien, but in many cases, you could pay $10,000 or less and walk away with a house. All you are paying for is the property taxes!

In New Jersey, if you don’t pay your property taxes, they become a tax lien. The different counties in New Jersey then sell these tax liens at a county auction once per year.

You can buy someone’s delinquent property taxes, and they will then have to pay you back, at up to 18% interest, plus attorney fees and any other related fees.

What if a mortgage and credit card judgment is attached to the home and it’s not only property taxes that are owed?

Will you get stuck having to pay all this debt?

Nope, you are in the clear!

A property tax lien is the senior debt with all priority. Any debt under this senior debt gets eliminated by the property tax lien, which is why this type of investment is an investor’s dream come true.

Tip 13: Make a Budget and Pay Off Debt

Make a budget analysis to get a clear visual of your expenses. There are many apps that you can use or even a Google Spreadsheet Template to make your budget for free.

Once you make a budget, now start lowering your expenses. Your goal is to increase your available cash-flow (how much extra money you have each month). Scroll down through your budget and find ways to reduce your expenses, like by lowering your grocery bill. You can start using coupons and doing whatever it takes to achieve your cash flow goals.

Once you find extra money, now use either the debt snowball or avalanche method and pay off all of your credit card debts as a starting point.

After paying off your debt, now start putting this extra money into an IRA or one of your retirement accounts.

If you can’t afford to pay off your debt on your own, here you can explore debt relief programs.

Tip 14: How to Setup & Manage All My Investment Accounts?

Do I need to hire an expensive financial advisor to set up all of these retirement accounts and manage them?

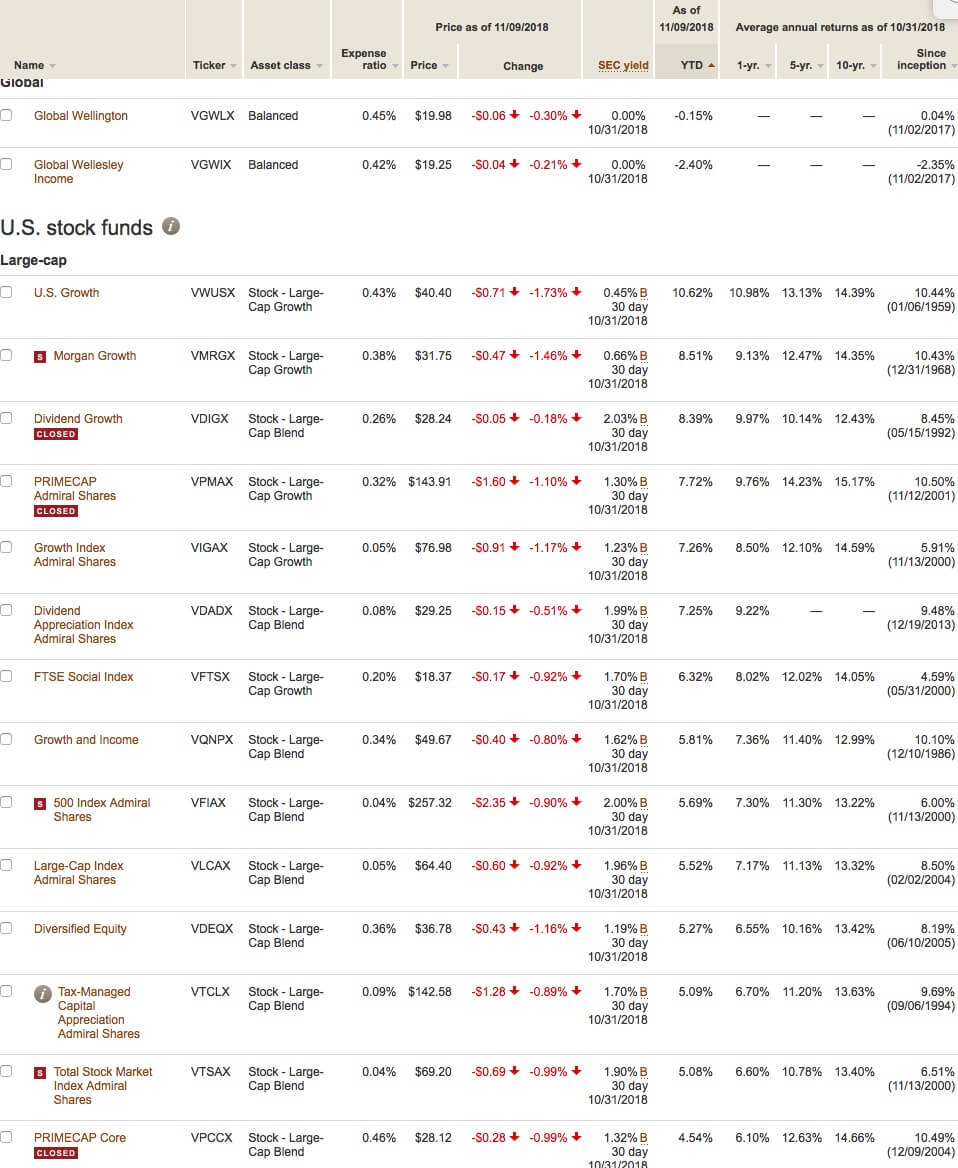

No, you can set up an account at Vanguard and invest on your own for free. It’s not that hard.

Vanguard offers Target Retirement Mutual Funds, which are age specific.

Vanguard manages what stocks these funds are made up of, so it’s kind of like having a financial advisor for free. Call Vanguard, and they will walk you through setting it up.

The older you are, the more conservative the investments will be, primarily consisting of bonds, instead of stocks. If you are young, Vanguard will invest more aggressively in stocks because they know that you have a longer time to achieve your financial goals.

The problem with having a financial advisor manage your funds is that they are usually very conservative in their investments, ensuring they play it safe to avoid losing money.

Keep in mind; financial advisors usually get around 1% of the total amount that they are managing as “their fee.” Financial advisors don’t get paid based on how much money they make you. Therefore, their objective is to keep your money safe and bring you a positive return.

In a firing market like today when interest rates are at a near all-time-high, you want to have your money in stocks. Stocks are where you can make the most money.

It’s easy to find out which mutual funds are performing best. Simply click on Vanguard’s page that says “all mutual funds” and voila! From there, sort the list by Year to Date (YTD) and start investing in the funds that have been making the most money over the last year.

Dive into what specific stocks make up each fund. You do this by clicking on any fund and then click on “portfolio and management.”

Once you get the list of stocks (companies), you can research each company to ensure it’s a safe investment.

Financial advisors will often allocate most of your budget into bonds, which are very safe, but you’ll be lucky to get a 5% return on your investment, which isn’t that great if you ask me.

Tip 15: Open a Health Savings Account (HSA)

A Health Savings Account (HSA) offers you a way to save for medical expenses and avoid paying federal income taxes on the money you invest.

Unlike a flexible spending account (FSA), HSA funds roll over and accumulate year to year if they are not spent.

Like the Roth IRA, after you receive your paycheck and the taxes are taken out, now you can invest this money into an HSA. But as the money grows with compound interest, you won’t have to pay a single cent in taxes on that growth; it’s tax-free.

With most retirement accounts you will need to start taking distributions at around seventy-in-a-half years of age, but with HSA’s you don’t have to.

If your contribution goes into an HSA (via payroll deduction), it is not subject to FICA rules and regulations. FICA, short for Federal Insurance Contributions Act, is the federal income tax that goes toward Social Security and Medicare.

Why this is important is because you can save an additional 7.65% with an HSA, compared to what you can save through your 401(k) and IRA. Just invest the funds from your bank account, into an HSA, and let your accountant figure out the math and how to document the details!

In 2018, the yearly limit that a person could invest into an HSA was $3,400, but for a family, that limit is $6,750. To qualify, you must be enrolled in a high-deductible health insurance plan (HDHP).

The IRS defines an HDHP for an individual as a plan with an out-of-pocket maximum of $6,550 and a minimum deductible of $1,300. For a family plan in 2017, the out-of-pocket maximum is $13,100, and the minimum deductible is $2,600.

You will receive a debit card or checks linked to your HSA balance, and you can use the funds on eligible medical expenses.

HSA’s do come with some restrictions and not every related medical expense is covered. For example, over-the-counter medicine is not covered by an HSA.

Also be aware that insurance premiums usually cannot be paid for with HSA funds.

Taxes and penalties. If you withdraw funds for non-qualified expenses before you turn 65, you’ll owe taxes on the money plus a 20% penalty. After age 65, you’ll owe taxes but not the penalty.

Most people have no idea about how to set up an HSA, but it’s relatively simple. All you need to do is ask your insurance company about it, and they will direct you on how to set it up, whether that be through them or if they use a third-party like a bank, credit union or financial advisor.

One of the most significant downsides to an HSA is if you don’t save enough to cover your medical expenses.

Tip 16: Start an LLC or Corporation if Running (ANY TYPE) of Business

Start a corporation or a limited liability company so that you can write off items including depreciation on your car, miles to and from work, office lunch, office supplies and much more!

If you are running any small business from your home, a limited liability company (LLC) protects you and your assets, just in case someone tries to sue you.

Here’s some additional information on how to set up an LLC and some of its benefits, from an article in entrepreneur.com:

Tip 17: Say Good-Bye to Student Loan Debt

If your income has been reduced this year, or even over the last few months, it’s time to consolidate your federal student loans and get on an affordable monthly payment. To consolidate your federal student loans, here are step by step instructions.

Once you consolidate your federal student loans, you can then get on an income-driven repayment plan that offers loan forgiveness. You only want to consolidate student loan debt and get on an income-driven plan, If you have a reduced income and strategically can come up with a plan to use the loan forgiveness laws to cut your debt down significantly.

When you get on a low payment through an income-driven student loan relief plan, the downside is that interest is still accumulating.

However, if you know that more than half your balance is going to end up getting forgiven at some point, then strategically, income-driven repayment plans can be your best solution.

Your monthly payment can be as low as zero dollars per month. And what’s best is that after 10-25 years, your remaining balance would get forgiven.

There are many cases where consumers will end up getting more than half of their debt forgiven. Plus, by consolidating you stay current on your monthly payments, and this is good for your credit score.

Teachers and police officers, and anyone working in a public service job can qualify for the Public Service Loan Forgiveness Program (PSLF). On the PSLF program, your student loan balance gets forgiven after only ten years.

If you have private student loans, refinance these with a low-interest loan. Or, you can contact a private student loan relief company to help you reduce your student loan debt.

As of 2018, new rules are being enforced regarding student loan relief. If you attended a college that is now shut down, you could be eligible to have your student loan debt discharged.

Where can I get financial advice?

Golden Financial Services offers debt relief for credit cards and student loans. We can get you a credit report, and if you have debt, we can provide you with options to get out of debt.

Call now for a free consultation at 866-376-9846.

You can talk with an IAPDA certified debt expert and get free financial advice today.

Keep in mind; Golden Financial Services is not a licensed financial advisor that charges a compensation. We can only help you with your unsecured debt, like with credit cards and student loans, but not with investing in the stock market. If you need a licensed financial advisor, contact one of the investment firms like Vanguard or Merrill Lynch, and many other reputable financial advisors can help you invest.

If you’ve enjoyed this post, check out 31 ways to get rid of credit card debt next:

Sources:

Investopedia, https://www.investopedia.com

The Balance, https://www.thebalance.com/best-budgeting-apps-4159414

Wikipedia, https://en.wikipedia.org/wiki/Compound_interest

Nerdwallet.com, https://www.nerdwallet.com/blog/health/what-is-an-hsa/

Entrepreneur.com, https://www.entrepreneur.com/article/72134

Bankrate, https://www.bankrate.com/finance/retirement/advantages-of-roth-iras-1.aspx