Ok let’s start at the beginning: A FICO credit score is a 3-digit number assigned to your purchasing habits and financial income that basically tells companies, potentially offering you loan types like mortgages, cars, and credit cards, what they would be getting into when approving or denying you. The FICO system takes several data points into account, like your revolving debt, your debt-to-available-credit ratio, how many hard and soft applications for credit you have made, and several other factors.

It is up to you to cultivate a solid number next to your social security number, but millions of Americans have no idea what their score is, or how to “build” positive credit. Many don’t even know that there are two main scores! Below we examine the correlation between your current credit score, and how it affects the next 5-1o years(ish) of your financial life.

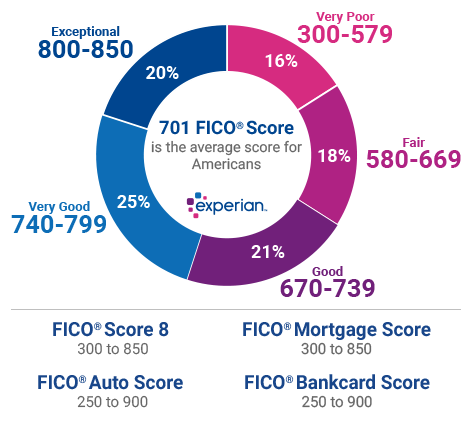

What Affects Your Credit Score the Most?

Your bill payment history. It’s not even ambiguous. There are actual percentage numbers attached to each factor (see the chart below). Your payment history makes up 35% Paying your bills on time and showing that you are responsible and on top of payments is the best way to show that you are capable of paying it back, with some interest.

Your total debt amount is the second-most important factor in your credit score, accounting for an additional 30% of your FICO score. In comparison to your payment history, there is a 1-to-1 ratio that makes your credit status very clear: That is, you have a reasonable amount of debt, and you make your payments on time.

The total level of debt you have is still very important, even if it’s the second-highest percentage in your credit score. TheBalance.com details this very well: “Credit scoring calculations, such as the FICO score, look at a few key factors related to your debt. The amount of overall debt you carry, the ratio of your credit card balances to your credit limit (also called credit utilization), and the relation of your loan balances to the original loan amount. As a guideline, you should keep your credit card utilization at 30% or less, meaning only charge up to 30% of any card’s available limit.”

How Does Your Payment History Impact Your Credit Score?

That 35% of your credit score has its own formula built into it, as a piece of a larger percentage. Weird right? It’s easier to understand when you consider your daily life. For example, if you opened a credit card over eight years ago, and you have managed to keep the balance under 30% while making all payments on time, that is considerably more valuable as evidence of responsibility than having three or four applications out for credit cards in the last two years. Having several credit card applications out at the same time shows that you might be having income troubles and are liable to miss payments.

Here is the rundown from CreditKarma.com: “Having a long history of on-time payments is best for your credit scores while missing a payment could hurt them. The effects of missing payments can also increase the longer a bill goes unpaid. So a 30-day late payment might have a lesser effect than a 60- or 90-day late payment.”

How Can a Positive Credit Score Impact Your Financial Life?

The price of your bills (especially car insurance), the down payment and interest rate on your first, second, third mortgage, decisions on loans, and even your personal relationships are all affected by your credit score, whether you even know what the number is or not.

The Anxiety and Depression Association of America reports that employment, income, and financial crisis makes up nearly 30% of all reported cases from psychiatrists in 2018. If your credit is terrible, you certainly aren’t alone. The key is to take a really long and thorough look at your finances (a Budget Calculator is excellent for this).

BusinessInsider.com puts some excellent perspective on all the ways a positive score opens doors. Especially important is their take on how your credit score influences your personal relationships:

“A recent Bankrate survey found that nearly four in 10 adults say knowing someone’s credit score will affect their willingness to date that person.

The Bankrate survey isn’t the only one to examine how a credit score could affect your relationships: A 2015 report from the Board of Governors of the Federal Reserve found that your credit score may affect who you end up with romantically and how long you’ll stay together — and the better the score, the stronger your relationship may be.”

Final Thoughts

If your credit is less than perfect, it doesn’t mean you will be stuck in a rut forever. There are ways to improve your credit score, little by little. There is no magic cure for overnight improvement of your FICO credit score, but establishing structure and a plan of attack can significantly retrain your brain to be more financially responsible. If you haven’t heard of the Debt Snowball Method, you might want to start there, after calculating your personal finances in terms of income-to-debt. The Golden Financial Services snowball calculator helps you begin to eliminate debt and free up cash flow, thus improving your credit score. Give it a try, and be sure to contact us for additional help!

____________________________

If you found our blog looking for financial advice or assistance with credit card debt relief or debt consolidation, call Golden Financial Services today at (866)-376-9846 or info@goldenfs.org. You can check out the rest of our blog here, and do your research on our services here. Let’s talk soon!