From SBA loan scams to Fintech Companies offering to Consolidate Credit Card Debt With Bad Credit, We’re About to Reveal What Borrowers Need to Beware Of. Millions of consumers have had a reduction in their income due to COVID-19. As a result, people are unable to afford credit card payments. Consequently, many consumers search for the closest thing that looks like a financial lifevest. And expensive credit card debt consolidation loan companies are throwing out lures everywhere.

There is a difference between a loan company offering expensive (or rip-off loans) versus a straight-up scam. Beware of both expensive loans and scams. And we will talk about both debt consolidation options that you want to avoid in the following blog post.

Mark Kantrowitz (@mkant), a Lending National Expert, says it best – “If you have to pay money to get money, it’s probably a scam.” Likewise, debt settlement programs that charge up-front fees before settling debt are also illegally operating. For debt settlement companies, fees can only be charged after a debt is settled and paid.

Should I consolidate credit card bills with bad credit?

The answer to this general question is that if you have bad credit and are looking to save money on credit card bills, a consolidation loan is probably not your best option. Instead, consider credit card relief programs, but first, understand the downsides that are included with each option. And make sure to use a licensed debt relief, accredited debt settlement, or non-profit consumer credit counseling company.

Alternatives to Consolidation Loans for Applicants with Bad Credit

Pay off high credit card bills by using the debt avalanche or snowball method, both do-it-yourself methods that will help improve credit scores and save money.

Steve Nicastro (@StevenNicastro), an expert in personal loans suggests; “Some lenders allow co-signers, which can help you qualify for a loan and get you a lower rate. Typically, the co-signer’s credit score must meet or exceed the lender’s minimum requirement. ”

If you do get a co-signer to help you qualify for a low-interest loan, as long as they add you as a joint account holder this option can benefit your credit score as positive payment history is reported on your credit report.

Is it smart to take out a personal loan to consolidate credit card debt?

Low-interest debt consolidation loans through credit unions are a smart choice. However, these low-interest credit union consolidation loans are only available for “good-excellent” credit applicants. Here’s where the Fintechs are cashing in. And by the way, Fintech stands for “Financial Technology.”

To compare less expensive credit card relief options, visit this page next.

Business Credit Card Consolidation SBA Loan Scams:

Struggling business owners are also falling victim to loan schemes. Credit card consolidators offer “SBA loans,” but through Fintech companies that charge outrageous upfront fees and interest rates. Small business owners need cash flow to pay their credit card debt. The credit card bills were accumulated by paying business expenses after the pandemic reduced business incomes. When a struggling business owner gets a phone call from a FinTech company that says they’re an SBA lender and can give them the cash within 24 hours, they’re quick to bite on the bait. These business owners would be better off focusing on a debt reduction plan to reduce their bills, a permanent long-term financial solution. Still, free money sounds more appealing to many. The problem is, it’s not free money that these loan companies are offering. This money comes with a hefty price tag.

Business credit card debt that is attached to a person’s social security number can qualify for debt relief programs in many cases. To find out if you’re eligible for a debt relief program call (866) 376-9846.

Can I use an SBA loan to pay off credit card debt?

“There cannot be any personal charges incurred on the credit card to be refinanced by the SBA 7(a) loan.” Click here for more information about SBA loans to pay off credit card bills.

How much does it cost to consolidate credit cards with bad credit?

Credit card consolidation companies (also know as Fintechs and online lenders) charge astronomically high interest rates when loaning to borrowers with sub-prime credit scores. On top of that, they also include upfront loan origination fees that can cost above 2-3% of the loan balance. So if you take out a $100,000 loan with a 30% interest rate and 3% processing fee, your monthly payment may be as low as $2,600, but over eleven years, you’ll end up paying $343,061 back (with the principle and interest). But not only that, in addition to paying $343,061 back, there will also be an upfront $3,000 fee, putting your total payback to over $346,061. Does that sound to you like a good deal?

Instead, consider paying the credit card debt back through a debt relief program, paying a significant amount less than $100,000, and saving yourself from ever having to file for bankruptcy. Try this online debt calculator tool to compare the savings on each debt relief program.

Details on how the credit card consolidation scheme works:

You think that you’re taking out a $100,000 loan, but the money that lands in your account may only be $97,000 or less. FinTech companies are making a fortune by processing these loans on behalf of banks and pocketing the processing fees.

Balance transfer cards for credit card consolidation:

The same occurs with balance transfer cards; credit card companies charge 3-5% of the amount getting transferred to the card as an upfront fee.

Before applying for a consolidation loan, make sure to read through the contract with a fine comb and do the math to figure out exactly how costly the loan truly is, adding up all fees and interest. Use a debt calculator to do the calculations for you.

As illustrated in the example above, it would take eleven years to pay back the $100,000 loan at $2,600 per month.

And with good payment history, you may get rewarded with more debt if not careful:

The same debt consolidation company will later offer the borrower a cash advance or some other expensive loan product to replace the 30% loan that will take eleven years to pay off. The Fintech company will then charge more upfront processing fees and capitalizing the current interest owed into the new loan, making your debt grow even more.

The Fintech company will once again sell you on the dream of “free money in your account to pay off this existing loan and replace it with something better.” These online lenders are often not licensed lenders and use a bank’s lending license to offer loans. Their role is to provide marketing and sell the loan on behalf of the bank. It’s a highly profitable industry, funded by consumers with financial hardships that are already struggling to get out of debt. The only one benefiting here all along is the Fintech company. Borrowers are then eventually forced into bankruptcy.

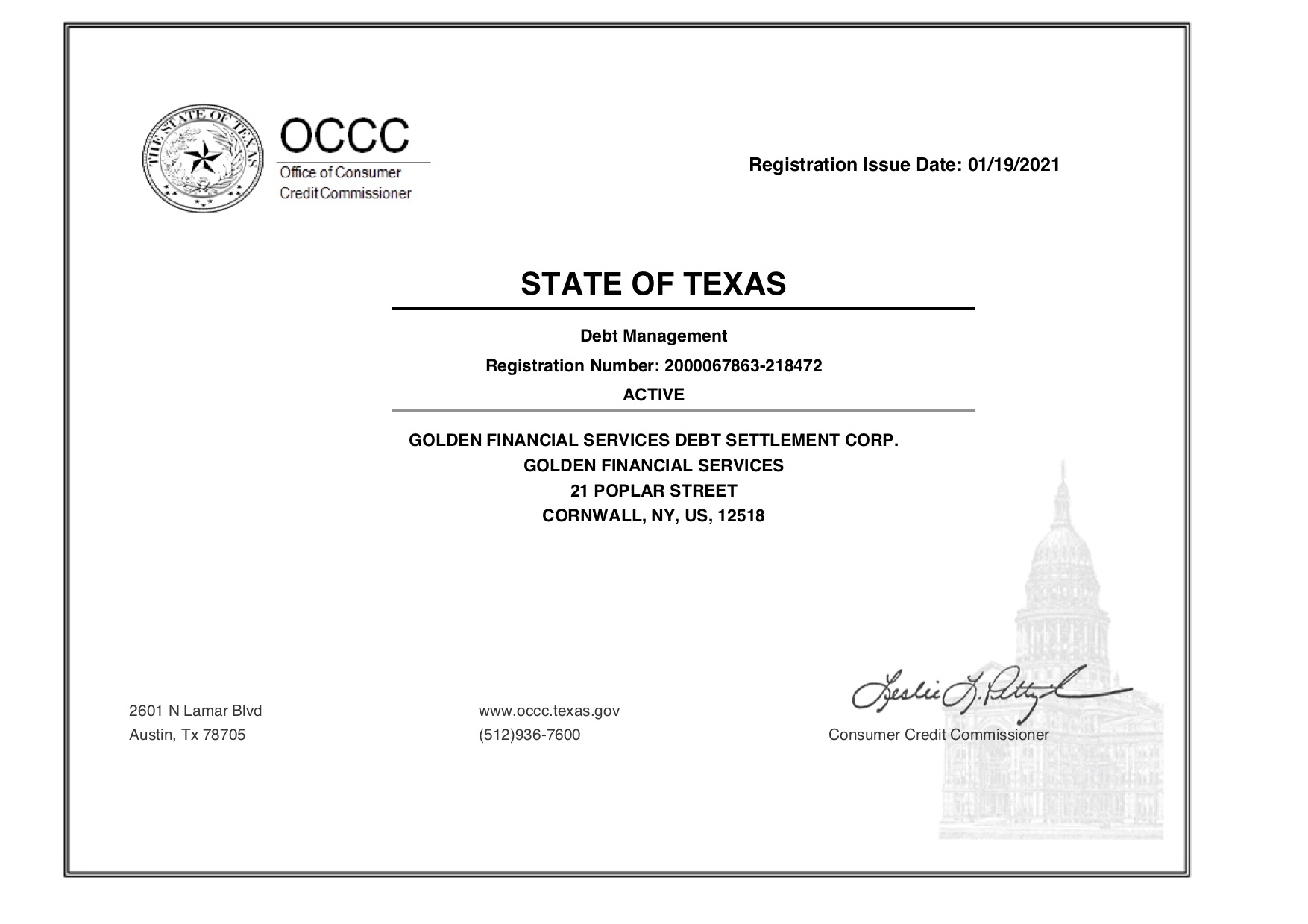

Is Golden Financial Services a licensed lender?

Golden Financial Services is a licensed debt management company, incorporated out of multiple states including Florida and Texas.

Check out this next article: “Golden Financial Loans – are they legit or a scam?”

What is the best way to consolidate credit card debt with bad credit?

Credit card settlement programs offer a less expensive route to becoming debt-free than credit card consolidation loans for applicants with low credit scores and bad credit. But these programs have their drawbacks, including the possibility of getting a credit card summons, that if ignored, could turn into a judgment.

A better option could be to join a debt validation program to resolve credit card debt that’s either in or going to third-party collection status, paying a fraction of what you’d pay when using a consolidated loan and less than the cost of debt settlement.

Click here to watch a credit card debt relief video and learn how to avoid scams—Call 866-376-9846 to find out about credit consolidation alternatives today.

Is it best to get a loan to consolidate credit card debt?

If a person’s credit score is above 675 and payment history is perfect, a low-interest loan may be the right choice.

This article offers the opinion of Golden Financial Services and only shares examples of loan schemes that we often hear from consumers. Not all online lenders and Fintechs are scams and fraudulent. This article is only attempting to educate consumers about fraudulent companies that offer expensive loans, bringing awareness to the subject. We purposely do not provide any specific names about companies because the consumer should do their research and calculations, making their own informed decisions.