Bankruptcy may be the only option available to solve your financial problems at times. Maybe you need to file for Chapter 13 bankruptcy to save your home from foreclosure or use Chapter 7 bankruptcy as an escape route to multiple credit card lawsuits. Or maybe your business is buried in debt and Chapter 11 bankruptcy is the only way to restructure its high debt payments. There are many legitimate reasons as to why a debtor may need to resort to bankruptcy.

What is bankruptcy?

Bankruptcy debt relief is offered through the federal court system and can help a person reduce or eliminate debt if they can’t afford to pay it any other way. Consequently, before a person files for bankruptcy they must complete a non-profit consumer credit counseling course to educate them on all debt relief options before a judge will consider someone qualified for bankruptcy.

Bankruptcy is considered “a federally mandated debt relief option” to help an insolvent business or individual either reduce or wipe away their debt. In other words, if a person has explored all of their debt relief options and still cannot afford to pay off their debt, a federal judge can restructure their debt payments with a Chapter 13 bankruptcy to be affordable or wipe away their debt with Chapter 7 bankruptcy.

On the positive side, bankruptcy is considered the fastest way to clear high debt, credit card lawsuits and simultaneously save a person’s home from foreclosure. On the downside, bankruptcy can leave a long-lasting negative effect on a person’s financial health.

Debt Settlement vs. Bankruptcy

It is imperative for a person to explore all of their options to get out of debt before contacting a bankruptcy attorney. Debt settlement could offer you a monthly payment as low as a Chapter 13 bankruptcy. However, debt settlement can be a faster debt repayment plan than a Chapter 13 bankruptcy because there is no pre-payment penalty with debt settlement and a person is not locked into a certain number of monthly payments.

For example, a consumer could sign up for a four-year-long debt settlement program and pay extra to graduate in under two years.

Many consumers do graduate from a debt negotiation program in under three years. Debt resolution is another option that includes a combination of debt relief strategies, all with the goal of helping a person become debt-free in the quickest possible timeframe and avoid bankruptcy.

All of the information provided in this post is from Golden Financial Services, an IAPDA Certified debt relief company, combined with data from reputable sources like UsCourts.gov.

To learn all of your debt relief options speak with a debt counselor for a free consultation at (866) 376-9846.

Additional Resources for Bankruptcy Alternatives

- Attorney-based debt negotiation program

- Compare pros and cons of credit card debt relief programs

- 10 Best Ways to Quickly Clear High Credit Card Balances

- Debt resolution that can invalidate collections accounts and remove debts from credit, (which also includes debt negotiation tactics)

Searching for a bankruptcy attorney near me?

Think twice before calling the first attorney that you find online after searching for “a bankruptcy lawyer near me.” These attorneys that advertise on the top of Google pay thousands of dollars per day to have their company listed at the top of Google. Consequently, they are probably not the cheapest bankruptcy attorney.

Start by contacting a licensed debt management or non-profit consumer credit counseling company. Golden Financial Services is a licensed debt management provider and can go over all of your debt relief options before you turn to that first bankruptcy lawyer online that’s only going to offer you bankruptcy.

Get a Free Consultation Today at Golden Financial Services at (866) 376-9846.

Consider bankruptcy alternatives: You may not need to file for bankruptcy, especially if your main concern is unsecured debt and credit cards. Bankruptcy could have a worse negative effect on credit scores and end up being more costly in the end, when compared to a debt resolution program.

You could resolve your debt for a fraction of what’s owed. And in many cases debt can get invalidated and removed from credit reports, rather than going in the opposite direction and filing bankruptcy, especially over credit card debt.

What’s the Difference Between Chapter 7, 11, and Chapter 13 Bankruptcy?

First and foremost, the main difference between Chapter 7 and Chapter 13 bankruptcy is that Chapter 7 lasts for 3-6 months and you don’t have to pay your debts back, while Chapter 13 continues for 3-5 years and you will pay at least half of your debt back.

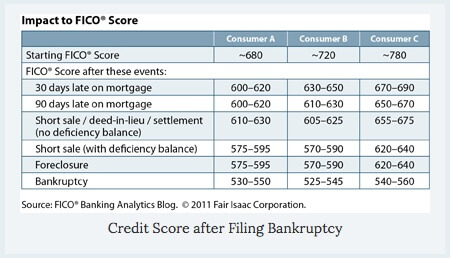

Did you know that “not all bankruptcies have the same effect on credit scores”?

With chapter 7 bankruptcy (also known as “liquidation bankruptcy”) a debtor’s assets are sold, and the proceeds are used to pay off creditors. However, 95% of debtors do a “no asset filing” because they don’t have any assets to be sold. If a debtor doesn’t have any assets to get sold, their debts are discharged and no longer legally owed.

What does discharged mean?

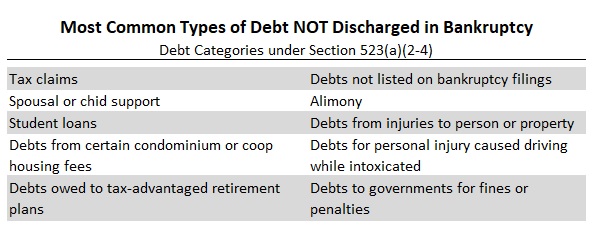

Credit cards, private student loans, medical bills, and almost all unsecured debts can get discharged and wiped away clean (excluding federal student loans, tax claims, spousal or child support, condominium and housing fees, alimony, and a few others).

Debts NOT Discharged in Chapter 7 Bankruptcy

Chapter 13 Bankruptcy

With chapter 13 bankruptcy (also known as the “wage earner’s plan”), the debtor pays at least half of their debt back over three to five years, depending on what the judge feels is “affordable to pay.” Chapter 13 bankruptcy is very similar to a consumer credit counseling program or using a debt consolidation loan to pay off debt (minus the adverse effect on credit with these two debt relief options).

With a debt consolidation loan, the loan pays off all of your existing debts, leaving you with one consolidated loan to pay back. With consumer credit counseling, you make one monthly payment to the consumer credit counseling company, and they disburse the funds to each credit card company every month but at a lower interest rate.

Do you have a monthly payment with Chapter 13 bankruptcy?

With Chapter 13 bankruptcy, you make one monthly payment to your bankruptcy trustee, and the trustee then distributes the monthly payments to each of your creditors.

Benefits of Chapter 13 Bankruptcy

Chapter 13 bankruptcy can save your home from foreclosure, allowing you to continue making your monthly mortgage payments. However, if late on mortgage payments during this second chance, your home could then be foreclosed on.

Another benefit of chapter 13 bankruptcy is that any debt due to a divorce can get reduced or dismissed.

In many cases, consumers apply for chapter 7 bankruptcy, fail the income means test, and get pushed into Chapter 13.

Hiring a bankruptcy attorney

Before you hire a bankruptcy attorney, speak to a non-profit consumer credit counseling program or a company like Golden Financial Services (GFS).

At GFS, we can check your debt relief options. There is a good chance that you’ll qualify for an attorney-based debt resolution program that can reduce your unsecured debt, providing you with increased cash flow and one low monthly payment.

Also important to note, with the attorney-based debt resolution program you’ll be assigned an attorney and worst-case scenario that attorney can help you file for bankruptcy. However, if you go straight to a bankruptcy attorney that doesn’t offer debt relief programs, that attorney won’t explore all available options with you and will of course guide you into the one option that they recommend (i.e., bankruptcy).

Call one of the debt specialists at Golden Financial Services for a Free Consultation today. Call (866) 376-9846.

How does bankruptcy affect credit?

- Bankruptcy can lower your credit score by at least 175 points

- It is noted on your credit report that you filed for bankruptcy and next to each creditor that gets discharged it will say, “debt discharged due to bankruptcy”

- Potential employers, landlords, and creditors will all be able to see that you filed for bankruptcy and could reject you from employment and renting a home

- Credit scores will be subprime after filing for bankruptcy, making it difficult to get approved for any type of credit in the future

- If approved for any type of credit after filing for bankruptcy, interest rates will be at their highest

- Premiums on car insurance, cell phone, and insurance monthly payments can all legally increase once bankruptcy goes on a person’s credit report

- The main difference between Chapter 7 and Chapter 13 bankruptcy is that Chapter 7 can stay on your credit report for 10-years versus Chapter 13 negatively affecting your credit for 7-years

Graph From FICO Illustrating How Bankruptcy, Short-Sale, Foreclosure, and Late Mortgage Payments Can Affect Credit Scores

If you’ve decided that Chapter 7 bankruptcy is your only option, here are the three primary phases that you need to get familiar with.

How to File for Chapter 7 Bankruptcy

PHASE 1: – Filing for Chapter 7 Bankruptcy

- The debtor must illustrate proof to the court of all income, expenses, debts, leases and financial affairs. You do this by filing a petition. You’ll need to submit A. completed bankruptcy forms and schedules B. creditor matrix (creditor mailing list, required in order to notify your creditors about the bankruptcy) C. credit counseling certificate and debt repayment plan D. pay bankruptcy courthouse filing fees (approximately $335, not counting attorney fees)

- You’ll need to get a certificate from a consumer credit counseling company. The credit counseling company must be approved by the government. A credit counselor will go over your other debt relief options. If you have credit card debt they will offer you a debt relief program where they consolidate credit card payments into a single payment and reduce all of the interest rates, allowing you to get a smaller monthly payment. If the credit counseling company can lower your credit card payments by enough, that will give you sufficient monthly cash-flow to avoid bankruptcy – that’s the goal. However, if the credit counselor sees that no debt relief program will help you at this point and you don’t have much-unsecured debt, they will recommend that you file for bankruptcy and even help you file.

- Before you qualify for chapter 7 bankruptcy you must pass the means test (where most debtors get pushed into Chapter 13 bk). If your household monthly income over the last five years, after accounting for a few allowed expenses, is more than $10,950 or 25% of the non-priority unsecured debt, you may not be allowed to file Chapter 7 bankruptcy. This is a test of your income. If your income is too high for chapter 7, the means test will require you to do chapter 13 bankruptcy where you pay at least half your debt back over 3-5 years. If a person’s “current monthly income” is more than the state median income, the debtor must take a “means test” to determine whether the chapter 7 filing is presumptively abusive.

PHASE 2: – Filing for Chapter 7 Bankruptcy

Immediately after submitting your bankruptcy petition at the courthouse, an Automatic Stay Order will stop most collection efforts directed at you and your property.

If you have credit card companies calling and harassing you, these calls will stop.

PHASE 3: – Discharge

- A few days after filing the petition, you’ll receive some paperwork in the mail. The paperwork will have your bankruptcy case trustee’s information on it, who will oversee your bankruptcy estate. When someone dies they get an estate that is managed by an executor. Bankruptcy is similar, but with bankruptcy, your estate is managed by a bankruptcy trustee. You will provide proof of income and all of your creditor’s information to your trustee. You can also think of a bankruptcy trustee like an IRS auditor. They will need to see everything, don’t try hiding any income from your bankruptcy trustee because they will find it and you’ll end up paying the price!

- You will have a meeting with your creditors and bankruptcy trustee, in front of the court where you’ll need to swear under oath and answer questions about your debts. If they catch you in one small lie that could disqualify you for Chapter 7. Even if it’s not an intentional lie, any wrong answers get treated as if you lied. Your creditors will use what you say against you down the road. (i.e., if a debt gets discharged, many years later your creditor could come back and force you to be liable for that same debt if they find out you provided inaccurate information at the creditors meeting) The most important thing to remember when trying to get approved for Chapter 7 bankruptcy is to just be honest and take your time prior to the creditors meeting to gather accurate facts and proof.

- Within 60-90 days after the meeting with your creditors, at that point the judge orders a discharge and sends a “Discharge of Debtor” notice to you and your creditors where your debts are all discharged.

Additional Information on Chapter 7 Bankruptcy That You Need to Know!

- A debtor can request for certain debts to be exempt. For example: if a person wants to keep their car, they can “reaffirm the debt” (a legal agreement between you and your creditor, letting you pay the debt).11 U.S.C. § 524(c).

- Simply filing a petition under Chapter 7, automatically stops all collection activity, including creditor phone calls, lawsuits, and wage garnishment 11 U.S.C. § 362.

- If a debtor has no assets to liquidate, creditors may not get paid anything. If the debtor does have assets to liquidate, all assets go into an estate. The estate becomes the new owner of the debtor’s property. The debtor’s creditors get paid from the nonexempt property of the estate.

- The main purpose of a Chapter 7 trustee is to sell and liquidate the debtor’s non-exempt assets from the estate, in a manner that maximizes the return to the debtor’s unsecured creditors. The trustee accomplishes this by selling the debtor’s property if it’s free and clear of liens.

- Unsecured creditors (i.e., credit card companies) must file their claims with the court within 90 days after the first date set for the meeting of creditors.

- A bankruptcy discharge does not extinguish a lien on the property.

- Filing a petition under Chapter 7 bankruptcy will result in the loss of certain assets and property.

- Each debtor in a joint case (both husband and wife) can claim exemptions under the federal bankruptcy laws. 11 U.S.C. § 522(m).

Eligibility Requirement for Chapter 7 Bankruptcy

- If a person’s “current monthly income” is more than the state median income, the debtor must take a “means test” to determine whether the chapter 7 filing is presumptively abusive. Abuse is presumed if the debtor’s aggregate current monthly income over 5 years is more than $12,850, or (ii) 25% of the debtor’s nonpriority unsecured debt, as long as that amount is at least $7,700.

- A debtor must first complete a credit counseling plan with a state-approved credit counseling agency 11 U.S.C. §§ 109, 111 before they’re allowed to file for any type of bankruptcy. A certificate will be provided by the consumer credit counseling company.

- Debtors must provide the assigned case trustee with a copy of their most recently filed tax return and proof of income.

- A person must file a petition with the bankruptcy court in the area where they reside.

- A debtor must complete the “Official Bankruptcy Form B22A”, entitled “Statement of Current Monthly Income and Means Test Calculation for Chapter 7 BK.” Download the official bankruptcy form here:

Filing Chapter 7 Bankruptcy (Cost and Fees)

- The cost to file for bankruptcy: $245 case filing fee, $75 miscellaneous administrative fee, $15 trustee surcharge (must be paid to the clerk at the courthouse)

- If the debtor’s income is less than 150% of the poverty level (as defined in the Bankruptcy Code), and the debtor is unable to pay the chapter 7 fees even over four installments, the court may waive the requirement that the fees get paid. 28 U.S.C. § 1930(f).

- $1,000 – $3,200 in attorney fees.

Best Alternatives to Chapter 7 Bankruptcy Include

[gfs-debt-calculator]

If you have delinquent unsecured debts:

Debt validation can dispute most third-party debt collection accounts. In many cases, debt collection companies can’t prove a debt to be valid and the debt becomes legally uncollectible. If a debt is legally uncollectible it doesn’t have to get paid and can no longer legally be reported on credit. Debt validation programs are accessible through Golden Financial Services at (866) 376-9846. Talk to an IAPDA certified debt counselor for free to learn your best debt relief option.

Debt settlement services can reduce unsecured debts by around 40%, before company fees. The part of the debt that gets reduced, is completely forgiven. Learn more about debt settlement services and how they can affect your credit here:

Consumer credit counseling can lower credit card monthly payments and interest rates, allowing a consumer to get out of debt in around 4.5 years. This type of program does not hurt your credit score. Click here to compare each debt relief program side by side.

Chapter 11 Bankruptcy: (business bankruptcy)

If your business is on the urge of getting sued and pending multiple lawsuits, it may cost you more than your business is worth defending. Plus, your business’s assets are at serious risk at this point. Chapter 11 bankruptcy can save your business from going down the drain and losing everything that it worked so hard to build over the years. Chapter 11 bankruptcy can also ensure your business stays separate from your personal credit and assets. You will be allowed to continue operating your business and the court will work out an affordable payment arrangement to help you pay back debt.

- The business remains active and avoids liquidation.

- A business’s debts can be lowered and the repayment period extended.

- A petition may be a voluntary petition, which is filed by the debtor, or it may be an involuntary petition, which is submitted by creditors that meet specific requirements. 11 U.S.C. §§ 301, 303.

- Protect personal assets

- Protect stockholder’s assets, other than the value of their investment in the company’s stock.

How to File Chapter 11 Bankruptcy, the Cost & Eligibility Requirements

- Must file with the court; listing all assets, liabilities, income, expenses, leases, and financial affairs.

- Must file a certificate of credit counseling and a copy of any debt repayment plan developed through credit counseling.

- Must provide a statement of monthly net income and any anticipated increase in income or expenses after filing, and a record of any interest the debtor has in federal or state qualified education or tuition accounts.11 U.S.C. § 521.

- Must pay $1,167 for the case filing fee

- Fees: $550 miscellaneous administrative fee

- Attorney Fees: $2,000 to $5,000 in attorney fees

Additional Information on Chapter 13 Bankruptcy (You Need to Know!)

- Just by filing the Chapter 13 bankruptcy petition, that action alone will automatically stop foreclosure, creditor phone calls, creditor lawsuits, and wage garnishment, just like with Chapter 7.

- Provides additional protection for co-debtors.

- The debtor must continue to make his/her mortgage payment while on a Chapter 13 bankruptcy, but at an affordable monthly payment.

- Allows individuals with regular income to repay all or part of their debts.

- If the debtor’s current monthly income is less than the state median income, the plan will be for three years. If the debtor’s monthly income is greater than the applicable state median income, the repayment plan will be for five years. 11 U.S.C. § 1322(d).

Chapter 13 Bankruptcy Eligibility Requirements

- Any individual, even if self-employed or operating an unincorporated business, is eligible for Chapter 13 debt relief, as long as the individual’s unsecured debts are less than $394,725 and secured debts are less than $1,184,200. 11 U.S.C. § 109(e).

- An individual cannot file Chapter 13, during the preceding 180 days, a prior bankruptcy petition was dismissed due to the debtor’s willful failure to appear before the court or comply with orders of the court, or was voluntarily dismissed after creditors sought relief from the bankruptcy court to recover property upon which they hold liens. 11 U.S.C. §§ 109(g), 362(d) and (e)

- Also, no individual may be a debtor under Chapter 13 or any Chapter of the Bankruptcy Code unless he or she has, within 180 days before filing, received credit counseling from an approved credit counseling agency either in an individual or group briefing. 11 U.S.C. §§ 109, 111.

- The main difference when filing a chapter 13 bankruptcy, is that the debtor must also “file a debt repayment plan” with the court since you are repaying at least a portion of your debts with Chapter 13. You then pay the case trustee, and the trustee disburses your payments to each of your creditors every month.

- A chapter 13 case begins by filing a petition with the bankruptcy court serving the area where you live. You must file with the court: (1) schedules of assets and liabilities; (2) a schedule of current income and expenditures; (3) a schedule of executory contracts and unexpired leases; and (4) a statement of financial affairs. Fed. R. Bankr. P. 1007(b).

- The debtor must also file a certificate of credit counseling and a copy of any debt repayment plan developed through credit counseling.

- The debtor must file evidence of payment from employers, if any, received 60 days before filing; a statement of monthly net income, and any anticipated increase in income or expenses after filing.

- A record of any interest the debtor has in federal or state qualified education or tuition accounts must be produced. 11 U.S.C. § 521.

- The debtor must provide the Chapter 13 case trustee with a copy of the tax return or transcripts for the most recent tax year as well as tax returns filed during the case (including tax returns for prior years that had not been filed when the case began).

- A husband and wife may file a joint petition or individual petitions. 11 U.S.C. § 302(a). The Official Forms may be purchased at legal stationery stores or downloaded from the Internet at: www.uscourts.gov/bkforms/index.html.

How to File Chapter 13 Bankruptcy, Cost, and Fees

- The courts must charge a $235 case filing fee and a $75 miscellaneous administrative fee. The fees must be paid to the clerk of the court upon filing. However, with the court’s permission, they may be paid in installments. 28 U.S.C. § 1930(a); Fed. R. Bankr. P. 1006(b); Bankruptcy Court Miscellaneous Fee Schedule, Item 8. The number of installments is limited to four, and the debtor must make the final installment no later than 120 days after filing the petition. Fed. R. Bankr. P. 1006(b).

- In order to complete all of the required Chapter 13 bankruptcy forms that make up the petition, statement of financial affairs, and schedules, the debtor must gather and produce the following:

1. A list of all creditors and the amounts and nature of their claims;

2. The source, amount, and frequency of the debtor’s income;

3. A list of all of the debtor’s property; and

4. A detailed list of the debtor’s monthly living expenses, i.e., food, clothing, shelter, utilities, taxes, transportation, medicine, etc.

Where to find a bankruptcy attorney?

You can visit the American Bar Association to find a reputable bankruptcy attorney.

https://www.americanbar.org/groups/legal_services/flh-home.html

Bankruptcy Forms: The United States Courts provide bankruptcy forms that are free for the public. UsCourts.Gov provides free bankruptcy forms for the public. http://www.uscourts.gov/services-forms/forms

Approved Credit Counseling Companies – Directory: Before a person files for bankruptcy they must complete debtor education and consumer credit counseling with a U.S. Trustee Program approved consumer credit counseling company.

By law, the U.S. Trustee Program does not operate in Alabama and North Carolina; in these states, Bankruptcy Administrators approve pre-bankruptcy credit counseling organizations and pre-discharge debtor education course providers.

To find a bankruptcy approved credit counseling agency, visit: http://www.uscourts.gov/services-forms/bankruptcy/credit-counseling-and-debtor-education-courses

For bankruptcy alternatives and credit card relief programs contact Golden Financial Services, an IAPDA certified debt relief company. Call (866) 376-9846 for immediate assistance!